In their simultaneously delivered budget speeches in mid-June, East African finance ministers struck a largely optimistic tone, projecting growth, focusing on improved livelihoods and emphasising their countries’ economic resilience.

Driven largely by GDP growth in Uganda, Ethiopia, Kenya and Tanzania – which together with Rwanda make up the five largest economies in the region – East Africa is set to register the highest regional economic growth on the continent. In 2023 and 2024 growth rates are projected to rise to 5.1% and 5.8% respectively from 4.4% in 2022.

At the same time, East Africa is facing an array of challenges: food insecurity, the worst drought in 40 years, protracted conflict in some parts of the region, high youth unemployment and a cost of living crisis exacerbated by the conflict in Ukraine.

In an increasingly uncertain global economic landscape post-pandemic, routes to recovery in the region remain unclear. Based on their recent budget speeches this blog looks at how finance ministries in the region are responding.

The 2023/24 budget speeches

As members of the East African Community (EAC), Uganda, Rwanda, Tanzania and Kenya share the same fiscal year. Finance ministers are expected to present their budgets simultaneously in June under a common theme.

In their recent budget speeches the Ugandan, Tanzanian, Kenyan and Rwandan finance ministers emphasised their economies’ resilience, positive growth and steady recovery as they recommitted to economic development with a focus on improving livelihoods. They also noted that growth had largely rebounded following the pandemic (Figure 2), driven primarily by growth in the services sector.

Nevertheless, the speeches did acknowledge potential pitfalls. All four ministers noted that recovery from the multiple crises facing the region required fiscal consolidation to reduce deficits and stabilise debt over the medium term.

Table 1: East African finance ministers

| Country | Minister | Budget speech date |

|---|---|---|

| Kenya | Njuguna Ndung’u | 15 June 2023 |

| Rwanda | Uzziel Ndagijimana | 15 June 2023 |

| Tanzania | Mwigulu Nchemba | 15 June 2023 |

| Uganda | Matia Kasaija | 15 June 2023 |

| Ethiopia | Ahmed Shide | 8 June 2023* |

Recovery and livelihoods

Inflation and the cost of living

In the largest East African economies inflation has been moderate relative to other sub-Saharan African countries, and to past levels. Even so, all five countries are seeing inflation trend upwards post-pandemic, primarily due to external shocks.

Domestic factors are also contributing in some countries, most notably in Ethiopia, where inflation has increased significantly over the last few years. While this was exacerbated by the conflict in Tigray, inflation has been one of the biggest policy concerns facing the country since the early 2000s.

Rwanda’s inflation rates have been volatile since 2019, and rose to 13.9% in 2022. In his budget speech, Finance Minister Uzziel Ndagijimana attributed this to fluctuating international commodity prices and a fall in domestic agricultural production.

Rising prices are particularly concerning for the region given high rates of poverty and inequality and limited social protection systems, particularly in Uganda. Both Tanzania and Rwanda announced new social protection measures.

Health and education

Despite the need for fiscal consolidation, the budget speeches also acknowledged the importance of improving outcomes in the health and education sectors, which were badly impacted by the pandemic.

The announcement of Kenya’s new five-year policy agenda, the Bottom-Up Economic Transformation Agenda (BETA), which aims to ‘stimulate the economy, bolster resilience while building on successes realised over time’, came with increases in budget allocations for health and education of 15% and 11% respectively.

Tanzania and Uganda allocated additional resources to health and education. However, the allocations for education in Tanzania, and for both health and education in Uganda, are at best keeping pace with inflation.

Rwanda announced several detailed social protection, education and health measures through the social transformation pillar of its National Strategy for Transformation (NST1) representing about 30.4% of the total budget for 2023/24. This was largely driven by an expansion in the education budget.

Table 2: Changes in health and education budget allocations (nominal)

| Country | Health | Education |

|---|---|---|

| Kenya | +15% | +11% |

| Tanzania | +13% | +5% |

| Uganda | +7% | +1% |

| Rwanda | -0.4% | +37.2% |

Fiscal consolidation

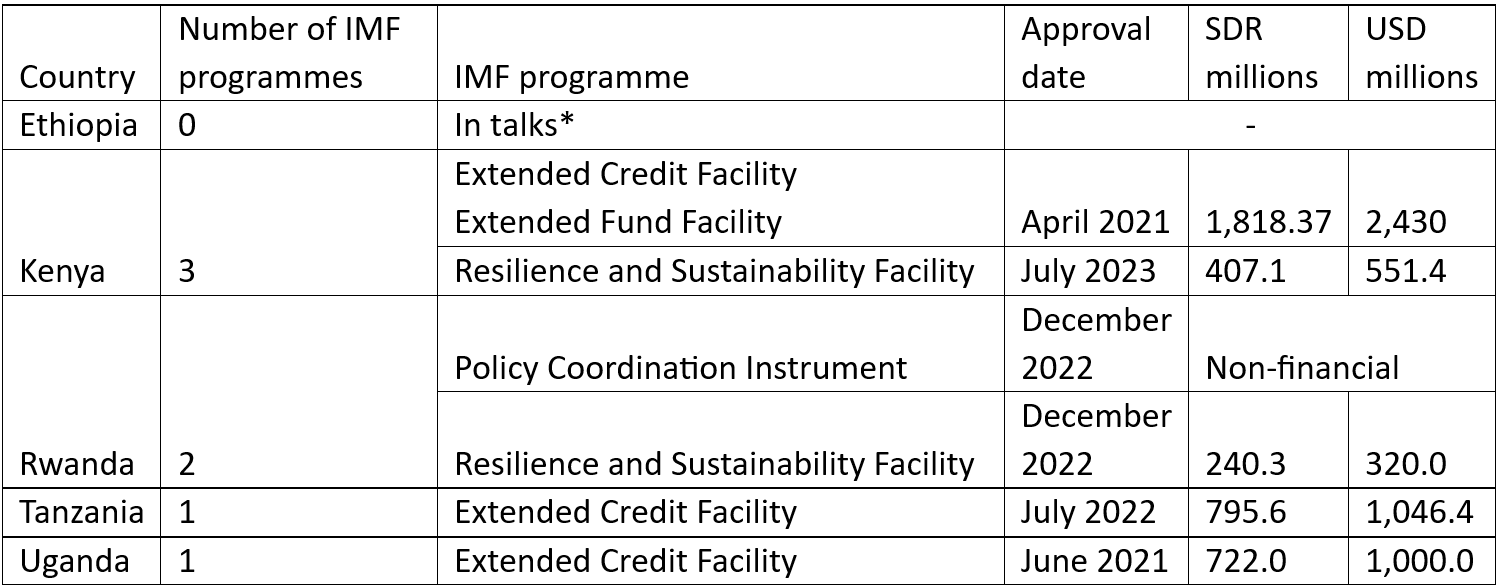

IMF programmes

IMF programmes in Kenya, Rwanda, Uganda and Tanzania underpin the focus on fiscal consolidation, while multiple news outlets have reported that Ethiopian authorities are in talks with the IMF to agree on a programme there.

Table 3: IMF programmes in East Africa

Revenue measures

Revenue-raising measures will be a major feature of fiscal consolidation in the region, through the introduction of new measures or widening of existing tax bases. Kenya, Uganda and Tanzania are all projecting increases in their revenue-to-GDP ratios in the coming years.

Tanzanian Finance Minister Mwigulu Nchemba used his budget speech to stress the importance of widening the tax base and reducing tax evasion.

For Kenya, Njuguna Ndung’u announced a myriad of revenue measures with the goal of increasing the revenue-to-GDP ratio from 15.1% in 2022/23 to 15.8% in 2023/24. These measures included the doubling of VAT on fuel and additional charges on electricity which have sparked protests and resulted in violence, highlighting the difficulties of managing the fiscal squeeze, in a context where civil servants’ wages were delayed for the first time since the country gained independence in 1963.

Similarly, in Uganda, Matia Kasaija announced the government’s intention to improve revenue collection from the 2022 level of 13.5% of GDP to between 16% and 18% over the next five years, by focusing on improvements to tax administration, fighting tax evasion and rationalising tax exemptions.

In Rwanda, the new IMF lending instrument, the Resilience and Sustainability Facility (see Table 3) saw its first set of budgetary implications. Notable among the revenue measures announced in the budget speech this year was an extension of the zero import duty incentive to accelerate the transition to electric vehicles.

Expenditure measures

Fiscal consolidation in the region will mostly be driven through expenditure measures. Nominal increases in total expenditure for 2023/24 have been modest across all five countries.

Table 4: Total expenditure 2022–2023 and 2023–2024, USD billions (nominal)

| Country | 2022/23 | 2023/24 | % change |

|---|---|---|---|

| Ethiopia | 14.2 | 14.7 | 1.9% |

| Kenya | 24.24 | 25.78 | 8.9% |

| Rwanda | 4.10 | 4.40 | 7.6% |

| Tanzania | 18.00 | 19.23 | 7.0% |

| Uganda | 12.93 | 13.90 | 9.6% |

As a result, total spending as a share of GDP is expected to contract across these countries, with the exception of Tanzania where it is expected to remain stable.

Kenya’s allocation to defence of approximately $2.3 billion for 2023/24 was almost double the previous financial year’s, and 34% more than its entire BETA agenda (which was allocated approximately $1.71 billion). Tanzania increased its defence spending by 11% from the previous year, to $1.87 billion for 2023/24. Ethiopia, Uganda and Rwanda have also stepped up military spending in recent years.

Deficits and debt

While the budget speeches acknowledged the need for fiscal consolidation, some finance ministers were less clear on the details.

The Kenyan and Ugandan finance ministries both projected lower deficits in 2023/24, down from 6.2% to 4.4% in Kenya and from 7.4% in 2022 to 5.1% in Uganda, with promises of convergence to the EAC target of 3% of GDP over time, and as early as 2026 for Kenya.

The fiscal deficit in Tanzania is set to be 2.7% in 2023/24, and like his Ugandan counterpart Finance Minister Nchemba also provided detailed estimates of public debt levels (his speech notably included the results of the recently concluded IMF Debt Sustainability Analysis) and outlined measures intended to ensure future debt sustainability.

Both ministers emphasised the need to prioritise concessional borrowing as a means to ensure debt sustainability. This strategy could however be difficult for Uganda, which in May 2023 passed one of the world’s harshest anti-homosexuality laws. As well as the legislation’s potential impacts on healthcare and tourism, the World Bank recently suspended new public financing operations in response. The budget speech made no reference to the legislation.

While Rwandan Finance Minister Ndagijimana acknowledged the importance of fiscal consolidation and debt stabilisation, he did not provide specific details on measures or strategies to achieve these goals.

Table 5: Key indicators

| Country | Fiscal deficit (% GDP) | Public debt (% GDP) 2022 |

|---|---|---|

| Kenya | 4.40% | Not available |

| Ethiopia | Not available | Not available |

| Rwanda | Not available | Not available |

| Tanzania | 2.7% | 32.5% |

| Uganda | 5.10% | 48.6% |

The most recent Debt Sustainability Analyses conducted by the IMF for these countries paint a concerning picture. The IMF considers both Ethiopia and Kenya to be at high risk of debt distress, while the other three countries are considered moderate risks.

Table 6 Debt Sustainability Analysis (DSA) for East African economies

| Country |

Risk of external distress |

Risk of overall debt distress |

Date of publication |

|---|---|---|---|

| Ethiopia | High | High | April 2020 |

| Kenya | High | High | December 2021 |

| Rwanda | Moderate | Moderate | January 2022 |

| Tanzania | Moderate | Moderate | July 2022 |

| Uganda | Moderate | Moderate | March 2022 |

Debt service costs have risen significantly in Ethiopia, Kenya, Rwanda and Uganda. According to the World Bank’s International Debt Statistics (IDS), debt service costs between 2020 and 2024 are projected to more than double in these four countries, growing by 526%, 112%, 106% and 204% respectively (Figure 8). Tanzania’s debt service cost grew significantly following the pandemic, but is projected to decline in 2024.

While Rwanda, Uganda, Tanzania and Kenya maintained their credit ratings, most received a negative revision in outlook from Fitch Ratings. The negative outlook is largely a function of limited availability of external financing in the face of increased domestic financing pressures. Tanzania was the only country assigned a stable outlook. Reflecting a very high risk of default, Ethiopia received a rating downgrade to CCC-.

Table 7: Credit ratings for East African economies

| Country | Fitch Ratings | Outlook | Date |

|---|---|---|---|

| Kenya | B (highly speculative) | Negative | 20 July 2023 |

| Ethiopia | CCC- (substantial credit risk) | Not assigned | 3 January 2023 |

| Rwanda | B+ (highly speculative) | Negative | 14 April 2023 |

| Tanzania | B+ (highly speculative) | Stable | 9 June 2023 |

| Uganda | B+ (highly speculative) | Negative | 24 March 2023 |

Questions for the years ahead

The optimism evident in the tone of the budget speeches reflects the post-pandemic growth rebound. However, deeper structural problems, ballooning debt and rising debt servicing costs have necessitated an aggressive fiscal consolidation across the region.

How can regional finance ministers determine an appropriate balance of fiscal consolidation measures while maintaining focus on socio-economic issues such as poverty, inequality and youth unemployment? Questions remain about how far fiscal consolidation can go without hurting the very people these policies aim to help.

Can the current post-pandemic growth rates be sustained given approaching headwinds and is private sector growth alone sufficient to improve livelihoods?

East African economies remain in a precarious position due to various external risks: a global economic slowdown, widening regional conflict, tightening of external financing and rising global food and energy prices.

Deft navigation will be required to successfully maintain equitable economic growth and stability in choppy waters.