The African Continental Free Trade Agreement provides a fresh opportunity for the development of the automotive industry in Nigeria through the development of regional value chains and supplier networks. Nigeria is widely considered one of the most promising economies in Africa, and its automotive industry is no exception due to both the large domestic market size and the large continental market that AfCFTA will offer. The industry gained prominence in Nigeria in the 1970s and 1980s, but was constrained by the high cost of domestic production and weak demand amid economic problems, currency volatility and the end of the commodity boom. As a result, the industry struggled to take off.

In our research, supported by the Supporting Investment and Trade in Africa (SITA) and UK Aid, we delve deeper into the nuances of the diverse possibilities of growth under the AfCFTA for the Nigerian automotive industry.

The State of the Automotive Industry in Nigeria

Today, Nigeria has a large and growing middle class base of about 50 to 100 million that could be potential buyers for automobiles, but it remains dependent on imports of new and used cars due to an inadequate domestic production to meet the rising demand. In 2021, imports of vehicles reached around $2.3 billion, 60% of which were passenger cars. Moreover, Nigeria is also a net importer of automotive parts and components mainly sourced from China, and South Africa, with a value of $4.5 billion in 2021. Clearly, this reliance on imports inhibits the development of a domestic automotive industry that may provide a positive spill over effects for other ancillary industries that provide raw materials to the production process. Other domestic constrains continue to deter the growth of the sector, including, energy costs, access to finance and inputs, and inadequate fiscal incentives.

Developing Local Production and Supply Chains

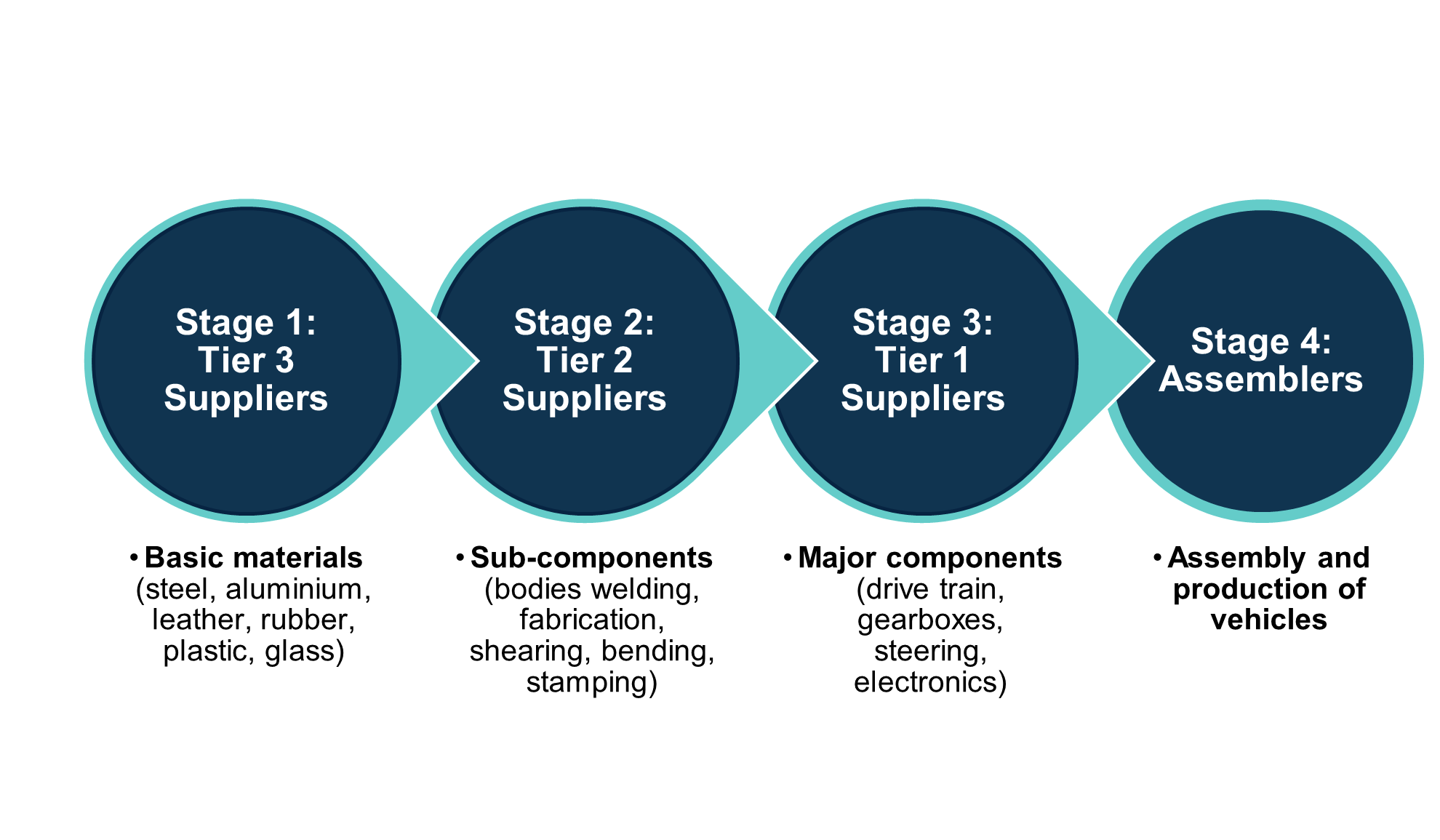

Nigeria can enter regional value chains that would lead to product and export specialisation in the auto sector. If Nigeria is interested in developing local production of vehicles, motorcycles and other two-wheelers, the government will need to implement directed policy interventions to enhance production capabilities, and develop an overall supply chain to create positive spill overs. Under a self-sufficiency condition, Nigeria would be compelled to develop the entire supply chain locally and sell the final product in the domestic market. This would be quite an expensive and inefficient production process for the Nigerian sector. Moreover, the lack of a domestic market would not justify large-scale investment in the sector. However, with modern trade opportunities, and the genesis of the AfCFTA agreement, Nigeria can enter regional or even continental value chains to assemble or produce fully-built units of vehicles, as well as parts and components, and then sell them in the consolidated and large African market (Fig X).

Figure X: Auto value chain: stages of production

Opportunities under the African Continental Free Trade Area (AfCFTA)

The Government of Nigeria should take advantage of the trading opportunities presented by the AfCFTA to develop the automotive industry through export promotion policies. The National Implementation Strategy of the AfCFTA in Nigeria aims to increase production of vehicles to 200,000 annually over a period of five years. Nigeria already exports trailers, semi-trailers, and pneumatic tyres to many countries on the continent and such Nigerian exporters are established suppliers for these products. Under the AfCFTA, Nigeria could export greater volumes of these products to achieve economies of scale. However, production and sale of automotives is governed by a heterogenous set of compliance issues that differ across countries. Harmonisation (full or even partial) of rules concerning environmental standards, passenger safety, and onboarding of suppliers along the value chain in line with international standards could benefit trade volumes.

Nigeria should improve the investment climate to attract foreign investors in the industry that could benefit from a large continental demand. The large internal market and prospective economies of scale could act as a signalling mechanism to foreign investors who wish to establish assembly and manufacturing plants in the country. Lessons can be drawn from successful cases on the continent (Morocco and South Africa) that relied significantly on foreign investment to supply vehicles to Europe and Africa. Perhaps Nigeria can follow suit once free trade (or some version of it) gets into full swing under the AfCFTA. This would require national and regional FDI liberalisation, and the creation of predicable FDI rules for the sector.

Nigeria can use the plentiful raw materials available on the continent to become an upstream producer of intermediate goods. A serious consideration should be given to the fact that most of the raw materials required to produce intermediate products in the sector, including lithium, aluminium and rubber, are plentiful in Africa. In theory, this could incentivise foreign investment too. Under the AfCFTA, Nigeria could form bilateral linkages with countries to exchange exports of raw materials and insert itself into upstream supplier networks. These raw materials could then be used to produce parts and components for the supply chain. Realistically, Nigeria has the potential to be a large supplier for parts to other countries such as Egypt, Kenya, Morocco, and South Africa.

The AfCFTA can be used as a collaborative platform by member states to enhance growth opportunities. Under the AfCFTA, the large and well-established players in the auto sector could also provide export training to new players in Nigeria wishing to join the value chain. Sharing of best practices, learnings, and experiences across not just national governments, but also large producers and assemblers would likely be a vital component of integration under the AfCFTA. However, policymakers in Nigeria must be mindful of the high minimum scale and investment required in vehicle assembly and component production. To this end, Nigeria will need to drive competitiveness to capture market share on the continent that could lead to economies of scale and increased efficiency.

The impact of Policy Interventions

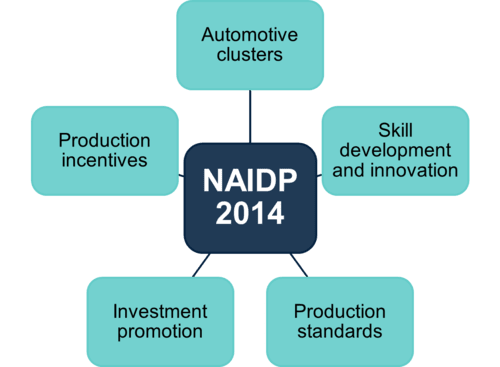

The ambitious goal will require directed policy interventions to establish the Nigerian auto industry and enhance its competitiveness. One such mediation was the National Automotive Industry Development Plan (NAIDP, see Fig Y) in 2014 that spurred growth in the industry and attracted $1 billion worth investments in the sector in 2019 alone towards increasing installed domestic capacity. Its successor, the NAIDP bill (Auto Bill), although facing uncertainty in its passage in the National Assembly, aims to provide a legal protection to OEMs wishing to invest in Nigeria, initiate a stable auto-policy environment and spur a multiplier effect to the rest of the economy by creating local supply chains.

Figure Y: Policy tools under the NAIDP (2014)

The competition from used vehicle imports “tokunbo” is a serious menace to any successful sectoral development. To make matters worse, the new Finance Act 2020 has reduced the import duty on Fully-build Units (FBUs) from 35% to 5%, while maintaining the duty of 10% on semi-knocked down (SKD) units that are imported by Nigerian assemblers. This move jeopardises the present and planned investments by assemblers in Nigeria, and discourages the assembly of complete knocked-down (CKD) units that could have initiated a move towards higher value addition in the sector.

Future Steps and Considerations

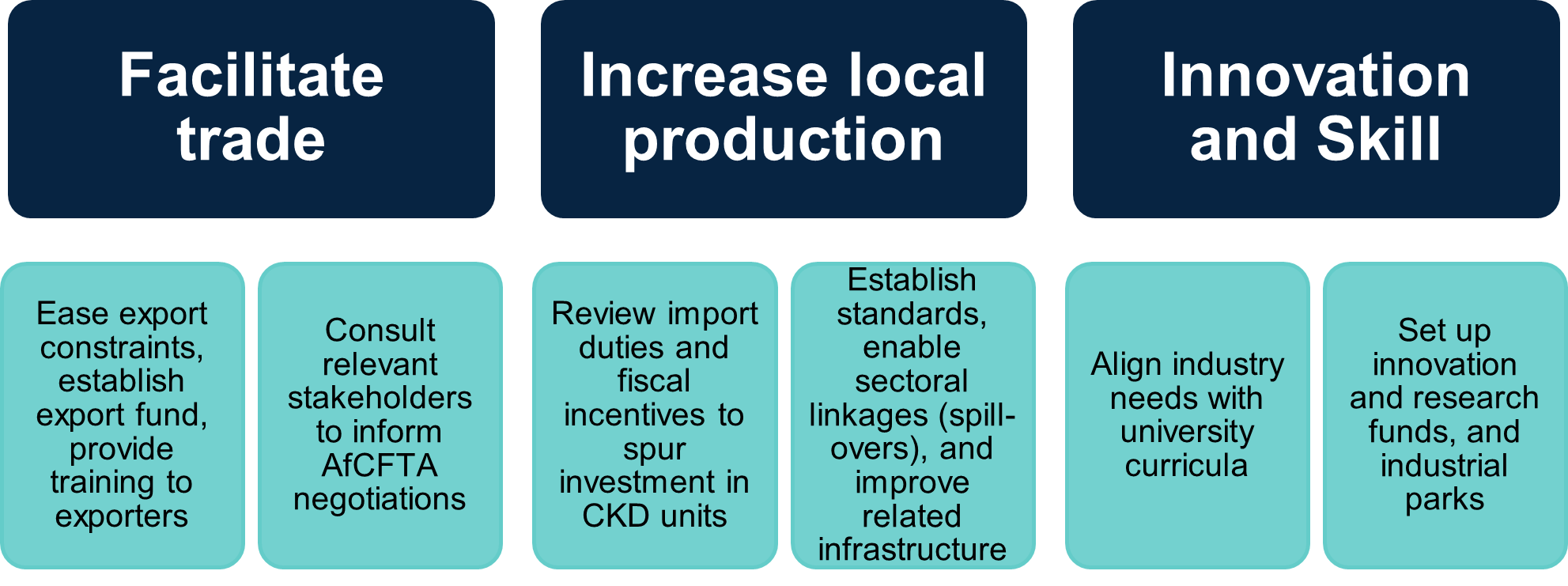

Future development will then depend on specific interventions to reduce or eliminate constraints affecting the growth of the automotive industry, including high energy costs and their unreliable supply, difficulty in accessing forex to import intermediates, a distorted fiscal incentive structure which reduces the returns to investment, low demand for vehicles, competition from imports, difficulty in accessing quality inputs, access to information, and access to finance. In this regard, collaborative efforts by the Nigerian Customs Service, Federal Ministry of Commerce and Tourism, Standards Organisation of Nigeria, Nigerian Export Promotion Council, and the Federal Ministry of Power, and other stakeholders, will be required to improve productive capacities and the investment climate for the automotive industry. Such policy interventions (see Fig Z) will need to be supported by efforts made by the auto producers and assemblers in Nigeria in the form of identifying export challenges and reporting them, taking advantage of the incentives to enhance competitiveness and exports, adhering to sectoral regulations, and investing in employee-skill nexus.

Figure Z: Policy recommendations for Nigeria

The government should also consider banning the imports of used cars over time, especially the old and accidented vehicles, and increase tariffs on such imports. Although with the current limited disposable income of the average Nigerian, the acute need for public transport, and limited access to car finance, imported used cars can still be critical for the living standards of most low-income Nigerians, the uptake in motorcycles as means of transport has reduced the impact of a complete ban that has the potential to spur domestic production. As banning used car imports may require a large political intent, it may be easier to increase the standards and regulations on such imports, along with higher tariffs to reduce their quantity and improve the quality of used cars on the Nigerian roads

Towards Inclusive Growth

The automotive industry is a contributor to industrial development in many African countries and has the potential to lift millions out of poverty. It is especially crucial for Nigeria’s economic transformation. Growth and development of the automotive industry is likely to have spill over gains in ancillary industries in the economy, including raw material producers of rubber, steel and aluminium. Recognising the poverty, climate and equality-related aspects of such industrialisation, Nigeria has an opportunity to work towards achieving sustainable development in its automotive industry under the AfCFTA. The AfCFTA Automotive Fund already aims to fast-track the development of the sector, locally and regionally. The Government of Nigeria must align its industrial and trade policy to the AfCFTA agreement and its initiatives to reap greater benefits of supporting local producers, creating value chains, supplier networks, and accessing a large internal market for vehicles, two-wheelers, and parts.

Read the complete analysis on the Nigerian Auto industry to delve deeper into how it can develop a domestic industry, while utilising the opportunities offered by the AfCFTA agreement.