In late 2020 the World Bank and the Asian Development Bank (AsDB) announced large-scale financing packages to help the rollout of Covid-19 vaccines in low- and middle-income countries. But despite the urgency of doing this to bring the global pandemic to an end, the uptake of these financing packages has so far been slow. Why are committed funds sitting idle at the same time that vaccination programmes are a priority in many countries battling new waves of Covid-19 infections? And at the same time as many activists and world leaders call on G7 leaders to ramp up their contributions to the global vaccination effort?

In this long-read we review some of the factors and bottlenecks that can plausibly explain this low uptake of MDB financing for vaccine purchases from governments in low-and middle-income countries. More importantly, we outline what management and shareholders of MDBs should do to ramp up the use of these financing facilities or deploy resources to support the health response against Covid-19. The fundamental issue has been between the country-based lending model of MDBs and the need to finance and procure a global public good (a low-cost vaccine). MDBs thus need a clearer mandate and dedicated grant financing for global public goods, including vaccine procurement.

1. What financing are MDBs providing for vaccine purchases?

Multilateral development banks (MDBs) responded to the Covid-19 crisis by scaling up their lending faster than bilateral donors. While infrastructure and the productive sectors have historically been the main areas of intervention of MDBs, many of these institutions have expanded their interventions to other sectors, including health. MDBs have well-oiled procurement and safeguarding processes, country offices with local access and knowledge, and they can mobilise resources at scale. It is no surprise, therefore, that MDBs have increasingly been involved in supporting and financing the vaccination rollout in many countries.

MDBs announced significant commitments to the vaccine rollout in low- and middle-income countries. Low- and middle-income can potentially access a total of $30 billion for the purchase and roll-out of Covid-19 vaccines across all these MDB facilities. This amount is not negligible. It’s equivalent to 34% of the combined annual average lending portfolio of the World Bank, AsDB and IADB, which amounted to $87 billion per year, between 2017/18 and 2019/20 (see Table 1 below for the World Bank and the AsDB). Most of these facilities were announced in late 2020:

- The World Bank has set aside a total of $20 billion to be deployed until the end of 2022 for the acquisition of vaccines (as part of the COVID-19 Strategic Preparedness and Response Program, or SPRP). Funding is equally distributed between the concessional window (IDA) and non-concessional window (IBRD). Funding was approved in two tranches, first in October 2020 and then in June 2021.

- Similarly, approved in December 2020 the Asia Pacific Vaccine Access Facility (APVAX) at the AsDB allocated $9 billion to support the procurement of vaccines and developing systems for distribution.

- Other MDBs – AfDB and IADB – have set aside resources for the Covid-19 response but either do not have a dedicated facility for vaccine purchases (the AfDB’s COVID-19 Response Facility announced in April 2020 is $10 billion but covers all facets of the response) or are proportionally much smaller than SPRP or APVAX (the IADB’s facility to support purchase and distribution of Covid-19 vaccines, announced in December 2020 is only $1 billion, not included in Table 1).

Uptake of these MDB facilities for vaccine procurement and distribution has been low so far. Figures have been steadily growing in the past months but 67% of the SPRP resources for IDA countries are yet to be allocated, 76% for IBRD countries; and 75% for AsDB’s APVAX facility.

Table 1: summary for MDBs facilities for vaccine procurement and delivery

| MDB | Average annual lending portfolio (FY18 to FY20) | Resources set aside for vaccine facility |

Resource committed so far |

% of commitments so far | Number of countries receiving funding | % total eligible countries |

| IDA (SPRP) | 6.9 (Grants); 18.4 (Concessional Loans) | 10 | 1.7 (Grants); 1.6 (Loans) | 33% | 46 | 62% (59 IDA countries and 15 Blend) |

| IBRD (SPRP) | 24.4 (Loans) | 10 | 2.4 | 24% | 15 |

21% (70 IBRD countries) |

| AsDB (APVAX) | 1.1 (Grants); 4.0 (Concessional Loans); 18.7 (Non-concessional resources | 9 | 0.1 (Grants); 1.6 (Concessional loans); 0.6 (Non-concessional loans) | 25% | 12 |

27% (45 countries with operations) |

Only 58 of the 92 mostly low and lower-middle-income countries eligible for the COVAX Advance Market Commitment facility (AMC 92) have so far agreed funding from at least one of the MDB facilities (it is worth noting that the World Bank IBRD’s SPRP and AsDB’s APVAX also provide financing to countries not eligible to receive vaccines from COVAX’s AMC mechanism). Furthermore, the allocation of MDB financing for vaccine purchases is highly concentrated in a few countries: nearly 38% of the financing packages agreed so far is for just three countries (the Philippines, Bangladesh and Pakistan), nearly 50% for just 5 countries and 66% for 10 countries.

2. Why aren’t countries demanding assistance from the MDBs for vaccine purchases?

Initial demand may have been low because the consequences of the crisis for demographically young low and middle-income countries were initially underestimated. This is a point that Amanda Glassman argued in her blog post in April analysing why the demand for World Bank financing for vaccines was so low. The fact that the first wave of the pandemic left many low- and middle-income countries relatively unscathed compared to Europe and the United States may have limited demand for vaccines. The finance ministries that need to commit funds may also have had doubts about the readiness of weak public health systems to distribute vaccines – e.g. the infrastructure for delivery is still in progress or not yet in place in parts of the country – which would lead them to delay commitments. However, the MDB facilities can be used to finance supply chain strengthening, and if this explanation was correct, we would expect to see high demand to finance this.

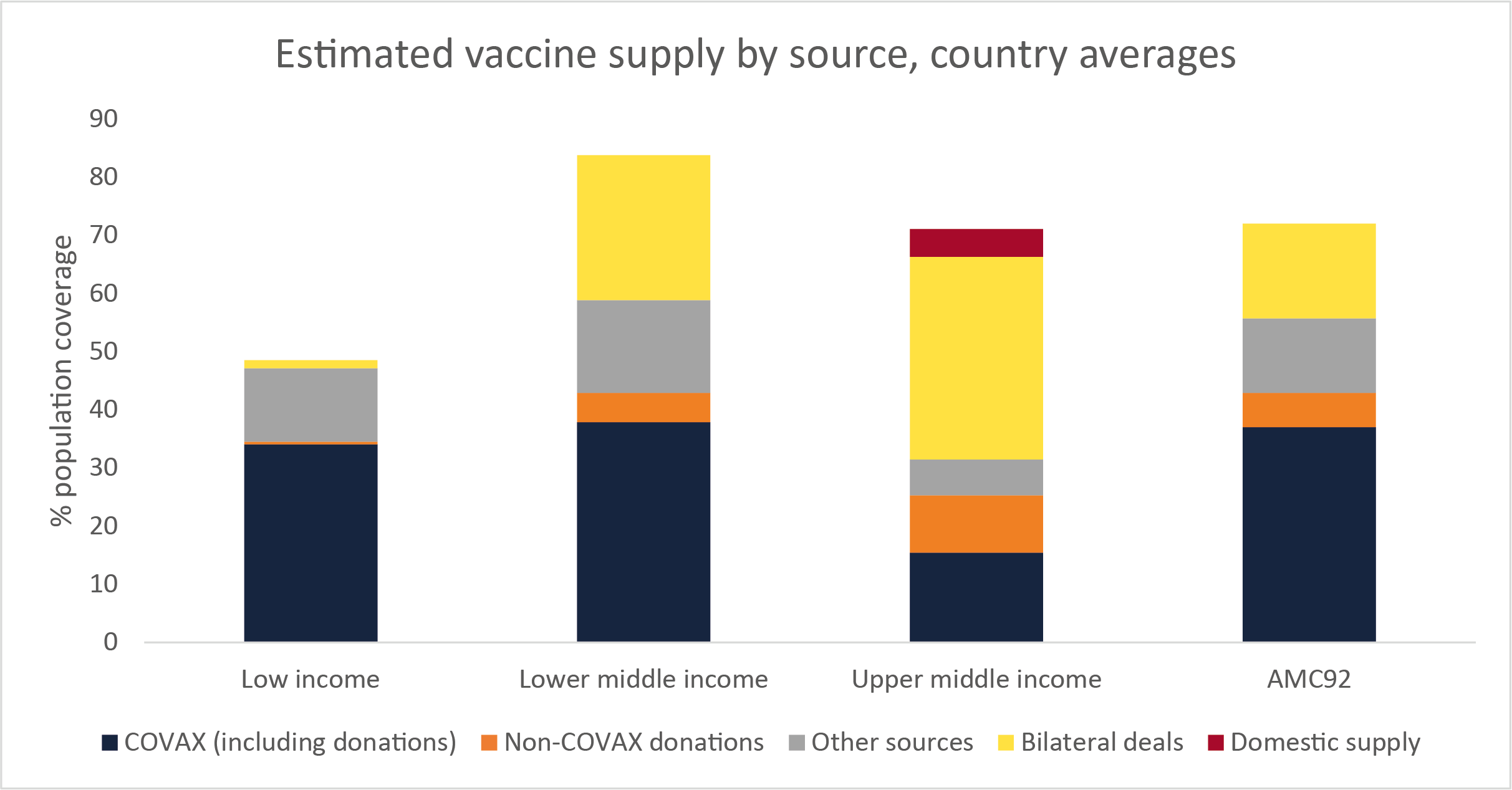

Countries have already purchased large volumes of vaccines using other revenue sources. Figure 1 below shows the average estimated secured supply of vaccines for each income group, and for the 92 countries that are part of the COVAX AMC. This demonstrates the different patterns of access to vaccines. For low-income countries, COVAX is by far the most important source of vaccines. But lower-middle and upper-middle income countries have invested significant amounts of their own resources in securing vaccines through bilateral deals. The vaccine supplies from ‘other sources’ which includes most World Bank-financed vaccines (whether through a bilateral deal, AVAT or the COVAX cost sharing mechanism) are of less importance.

Figure 1: estimated vaccine supply by source, country averages

The initial design of the MDB facilities may have made them unattractive to countries. While we do not have data on the timing of deals available, the initial restrictions on which vaccines the MDB funds could be used to procure, and which mechanisms could be used, may have made them unappealing. When the World Bank and AsDB initially launched their vaccine financing facilities, the only vaccines that could be purchased by countries with these facilities were those selected for procurement through COVAX, those prequalified by WHO or those authorised by at least three “stringent regulatory authorities” (SRAs). Recognising that these conditions were inappropriate, these were subsequently relaxed in April to make eligible any vaccines with WHO emergency use listing, plus any being procured by COVAX which are also authorised by at least one of the six SRAs (Australia, Canada, EU, Switzerland, US, UK).

Further changes were made in June and July to allow World Bank funds to be used in pooled procurement mechanisms. This has several advantages for purchasing countries, including drawing on the expertise of the organisations involved in COVAX, a diversified pool of vaccines, and access to advance purchase agreements. In June, the Bank agreed that funds could be used to purchase the vaccine supply secured by the Africa Vaccine Acquisition Task Team, and in July, it was agreed that AMC countries could use World Bank funds to procure additional doses from COVAX, allowing countries to take advantage of the advance purchase agreements COVAX has already negotiated. However, as figure 1 shows, only low-income countries are likely to need this additional funding to purchase additional vaccines.

Governments may also have been reluctant to finance additional vaccine coverage from borrowing. Evidence from looking at the financing transition as countries progress up the income per capita ladder from grants towards concessional and then non-concessional loans shows governments can be reluctant to borrow to finance social sector spending. This also includes expenditure in the health sector.

In their review of eight lower-middle income countries, Engen and Prizzon (2019) find that governments tended to be reluctant to borrow for ‘soft’ sectors – those related to human development, such as education, health and social protection. Loans were more likely to be invested in infrastructure development. This was also the case for decisions on financing rural development (Prizzon et al., 2020) and education (Rogerson and Jalles d’Orey, 2016). The same factors may apply to the case of vaccine financing if countries are reluctant to borrow for recurrent expenditure. On the other hand, borrowing at non-concessional terms from the MDBs is still cheaper for many market-access countries than borrowing from commercial sources.

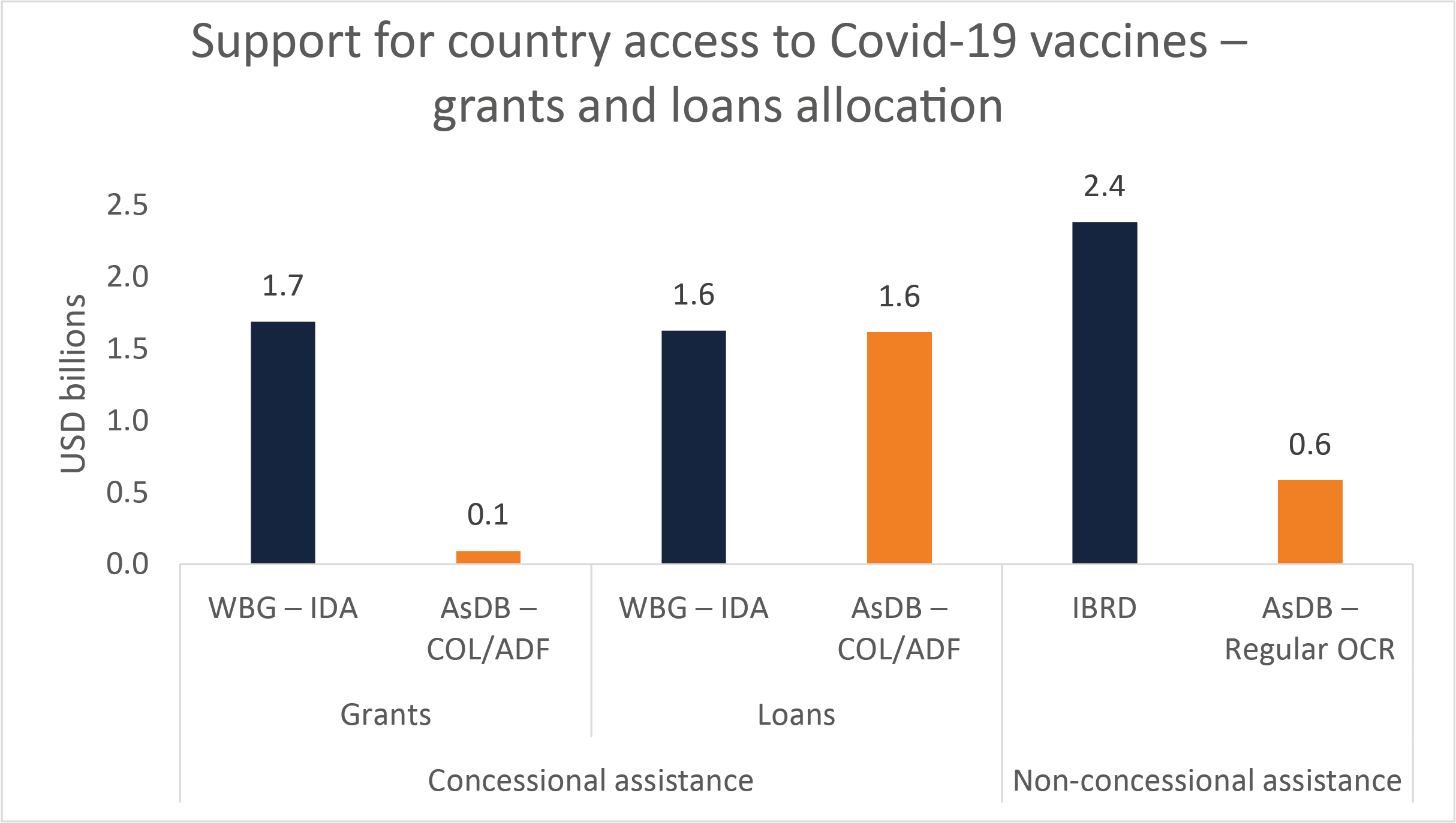

This interpretation is reinforced by the fact that there is higher demand for World Bank grants to finance vaccine purchase and roll-out than for loans. First, the grant-financed component of the IDA vaccine operations is 51%, nearly double the three year average share of grant financing across IDA projects (27%). Second, while 62% of IDA countries (borrowing at concessional terms or receiving grants) have received support for vaccine purchases so far, only 21% of IBRD countries have done so (those countries that can only borrow at non-concessional terms). This would call for terms of the loans for vaccine financing offered by MDBs to be softened, as argued by Justin Sandefur. An example is the Global Concessional Financing Facility to lower the terms and conditions of loans from non-concessional to concessional of middle-income countries that support both refugee populations and host communities.

At the Asian Development Bank, grants accounted for 21.5% of the average concessional portfolio between FY2018 and FY2020 but only 5.5% of funding approved for vaccine purchases under APVAX are grants in the concessional window (Figure 2). Why? Most of the demand for the APVAX facility has come from countries with large populations – i.e. Bangladesh and Pakistan – that are only eligible for concessional loans. Grant financing under APVAX has been relatively small so far – to Afghanistan, Tajikistan and Pacific Islands.

Figure 2: support for country access to Covid-19 vaccines – grants and loans allocation

A further concern Finance Ministries of IDA-eligible countries might have is the impact of allocating scarce IDA resources to vaccine purchase and roll-out. The funds the World Bank is earmarking are not new and must ultimately come from existing IDA resources. Use of these funds may thus have implications for the reallocation of the country financing envelope, and allocating them to purchase vaccines may mean depriving other priorities from funding.

Why are low-income countries not prioritising purchasing vaccines from their own resources or MDB funds? If a faster global vaccine roll-out is the key to economic recovery, it may seem perverse that this is not being prioritised by the world’s poorest countries. But putting yourself in the shoes of a low-income country finance minister could make this seem less so. Many of these countries are extremely fiscally constrained, and have had a much smaller fiscal response to Covid, despite seeing larger downgrades in their growth projections than higher income countries.

First, why use scare resources to purchase more vaccines now when supply has so far been so unreliable? Data from the Multilateral Leaders’ Taskforce on Covid-19 estimates that low-income countries have on average received less than 12% of the vaccine supplies they have secured. It is understandable that they may first want to wait to receive these vaccines before making new orders.

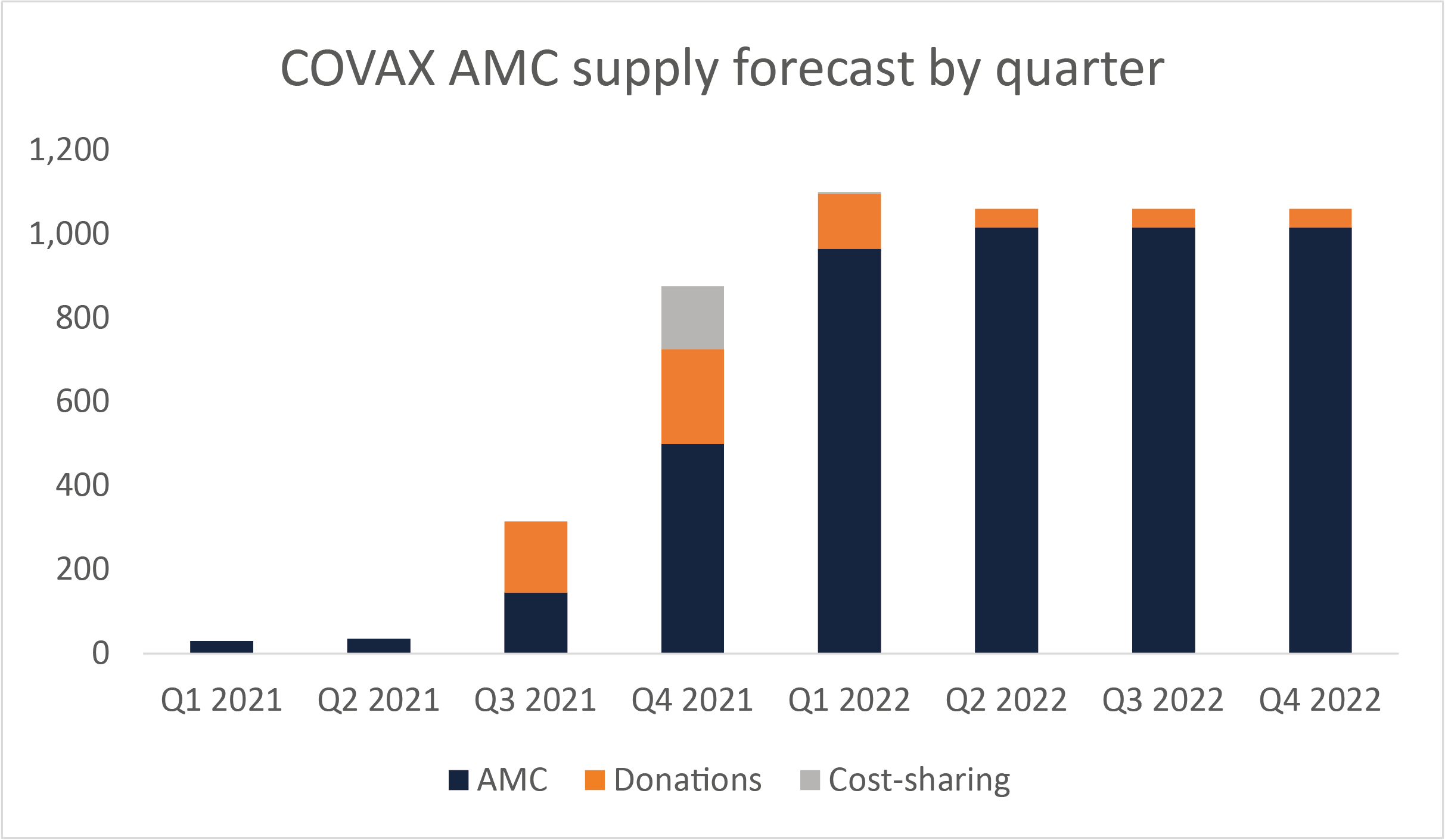

Second, Finance Ministers may want to wait and see how their health systems manage the challenge of delivering these vaccines before making new financial commitments. COVAX is forecasting a rapid rise in deliveries in the last quarter of 2021, with volumes almost tripling, and the first quarter of 2022 as shown in Figure 3 below.

Figure 3: COVAX AMC supply forecast by quarter

Third, low-income countries may be in line to receive more vaccines on a grant or donation basis. COVAX is forecasting available supply well beyond its existing commitments to provide sufficient vaccines for 30% of the population. It predicts it will be able to supply enough doses for 37% of the AMC91 countries’ populations (i.e. excluding India which due to its population size will receive a lower allocation) by end Q1 2022. Procurement of the potential supply beyond this “will depend on COVAX AMC fundraising, AMC92 cost-sharing beyond donor-funded doses, and the final prices and volumes of doses allocated to AMC92.”

Given this, low-income countries would seem to be in a position to see whether additional grant financing will come on stream – or alternatively, whether the new commitments by the US and EU at the US Global Covid-19 Summit last month to share a further 1 billion doses materialise. This may be preferable to reallocating their IDA portfolio, which may be at least partly in the form of loans rather than grants, depending on the country’s risk of debt distress.

This delay may also be beneficial as it allows countries to assess which vaccine candidates best suit their needs. In September, Novavax applied for WHO emergency use listing, and following positive large-scale trial results, Clover announced that it would do so before the end of the year.

3. What should be done now?

By putting funds at risk to secure access to vaccines that were still in development, high-income countries were first in the queue to receive approved vaccines. Low and middle-income countries typically do not have the fiscal capacity to do this. COVAX was meant to provide the pooled procurement capacity and expertise to do this for low- and middle-income countries. Unfortunately, it has failed to do this both because it did not have sufficient up-front funding, and because it was too reliant on a single source of production in the Serum Institute, that was then delayed when production was diverted to domestic demand after India’s winter surge in cases.

MDBs have stepped up their resources for vaccination, but there has been a mismatch between how funds have been made available, and where they are needed. MDBs have stepped up their grants and loans portfolios in response to the Covid-19 crisis and have dedicated resources to help low- and middle-income countries in the roll out of the vaccination programmes. But these facilities were initially poorly designed, unduly limiting the vaccines that were eligible for purchase, and not ensuring that the funds could be utilised through pooled procurement mechanisms that can obtain vaccines most efficiently, especially for countries with scarce technical expertise to evaluate vaccine candidates and contract with pharmaceutical manufacturers.

These problems are now being resolved, but a year too late, and at a time when the pandemic is still claiming lives in unvaccinated populations in many low- and middle-income countries. The new financing facility set up by the World Bank and COVAX in July 2021 now allows COVAX to make advance purchases from vaccine manufacturers using financing from the World Bank and other multilateral development banks, beyond donor-subsidised vaccines. The creation of this facility addresses some of the issues we have discussed here, linking demand for vaccines from governments and their financing from international financial institutions. However, this approach should be implemented systematically across MDBs and financing should be additional to the resources allocated to each country. MDB financing also needs to ensure countries are building up absorptive capacity as larger volumes of vaccines become available.

The priority now for the MDBs is to support roll-out of vaccines when they start arriving in quantity from COVAX and AVAT. The fact that contracted supply does not seem to be a major issue at the moment means the immediate focus must be on other issues. Key is going to be ensuring that secured doses are actually delivered to low and middle-income countries. To ensure this happens, the heads of the IMF, World Bank, WHO and WTO have called for countries with high vaccination coverage to swap their delivery schedules with COVAX and AVAT, to fulfill their donation commitments to COVAX, and for manufacturers to prioritise their contracts to COVAX and AVAT. Once these vaccines have arrived, they must be efficiently rolled out. At present the World Bank is by far the largest funder of support for vaccine delivery, providing over half of the $2 billion currently allocated to countries for this purpose (as of 23 September), according to data tracked by UNICEF. It must thus have a near-term focus on supporting countries to effectively utilise these funds to get jabs into arms.

But more broadly this crisis has once again shown that the country-based lending model of MDB does not generate the right incentives for the financing and procurement of global public goods. Future reforms will need to deal with the long-standing tension between the multilateral development banks being the best placed institution to finance global public goods, and their current country-based financing and resource allocation model. To address this for vaccines, the G20 High Level Independent Panel on Financing the Global Commons for Pandemic Preparedness and Response has recommended that the World Bank support countries to participate in pooled procurement mechanisms for advance purchase contracts and to allow countries to borrow beyond their country allocation.

Shareholders should give a clearer mandate and provide resources for the provision and grant financing of global public goods, including vaccine procurement. As Nancy Birdsall and Scott Morris eloquently argued in the 2016 High-level report on the future of multilateral development banking, “the lack of a mandate to raise and deploy grant resources to support GPGs” has been a major constraint in the financing and implementation of GPG-related projects. This applies to both concessional and non-concessional windows, but especially to the latter where loans are the only option.

The initially slow uptake of vaccine purchases in low- and middle-income countries shows how the Birdsall and Morris proposal to create a new financing window or fund with a separate governance structure and grant resources – especially at the World Bank – remains very relevant. The G20 High Level Independent Panel on Financing the Global Commons for Pandemic Preparedness and Response also argued for more grants from MDBs to support country and regional level investment in global public goods, with a core mandate on their provision.

It is now the time to revisit this discussion and address the tension between the country-level allocation model of the IFIs and the mandate for the provision and financing of GPGs.