In a previous entry on Budgets and Bytes we covered El Salvador’s decision to make Bitcoin legal tender. One of the stated objectives of this policy was to lower the costs of remittances. The experiment seems to have failed, for many reasons, and has had little to no impact on the flow of remittances into El Salvador.

Nevertheless, finding ways to lower the cost of remittances remains a major issue for development, which our Chief Executive Sara Pantuliano will be discussing at Davos this week. The stakes are high, the problems are well known, and solutions will require more action by governments, the private sector, and greater cooperation between both.

What’s at stake?

Remittances are a big deal for reducing poverty and financing development. They play a major role in normal times, and an even more significant role in response to economic shocks.

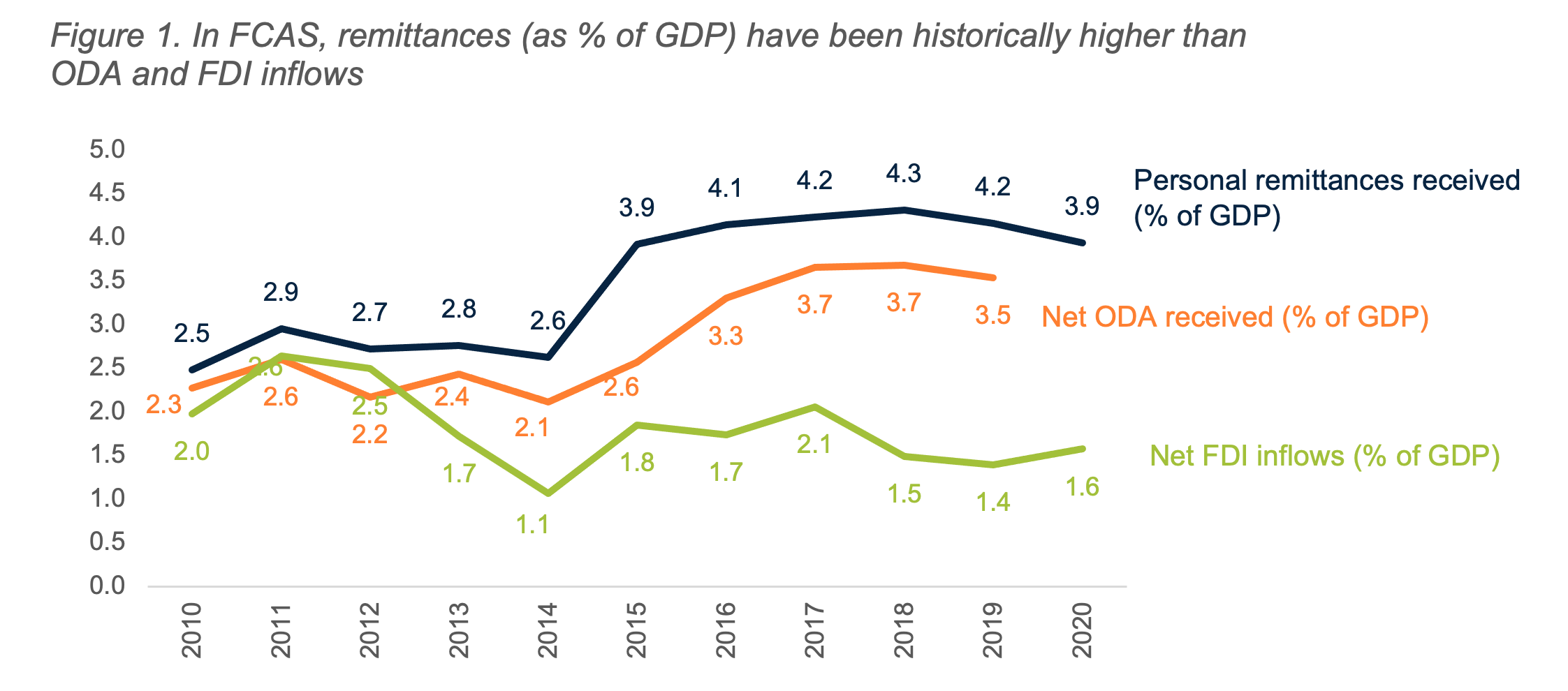

From a macroeconomic perspective remittances are a major source of external financing for many lower and middle income countries, and are often more important than official development assistance (ODA) or foreign direct investment (FDI) for fragile and conflict affected states (see Figure 1 below).

Source: Author’s computations based on data from World Bank Development Indicators.

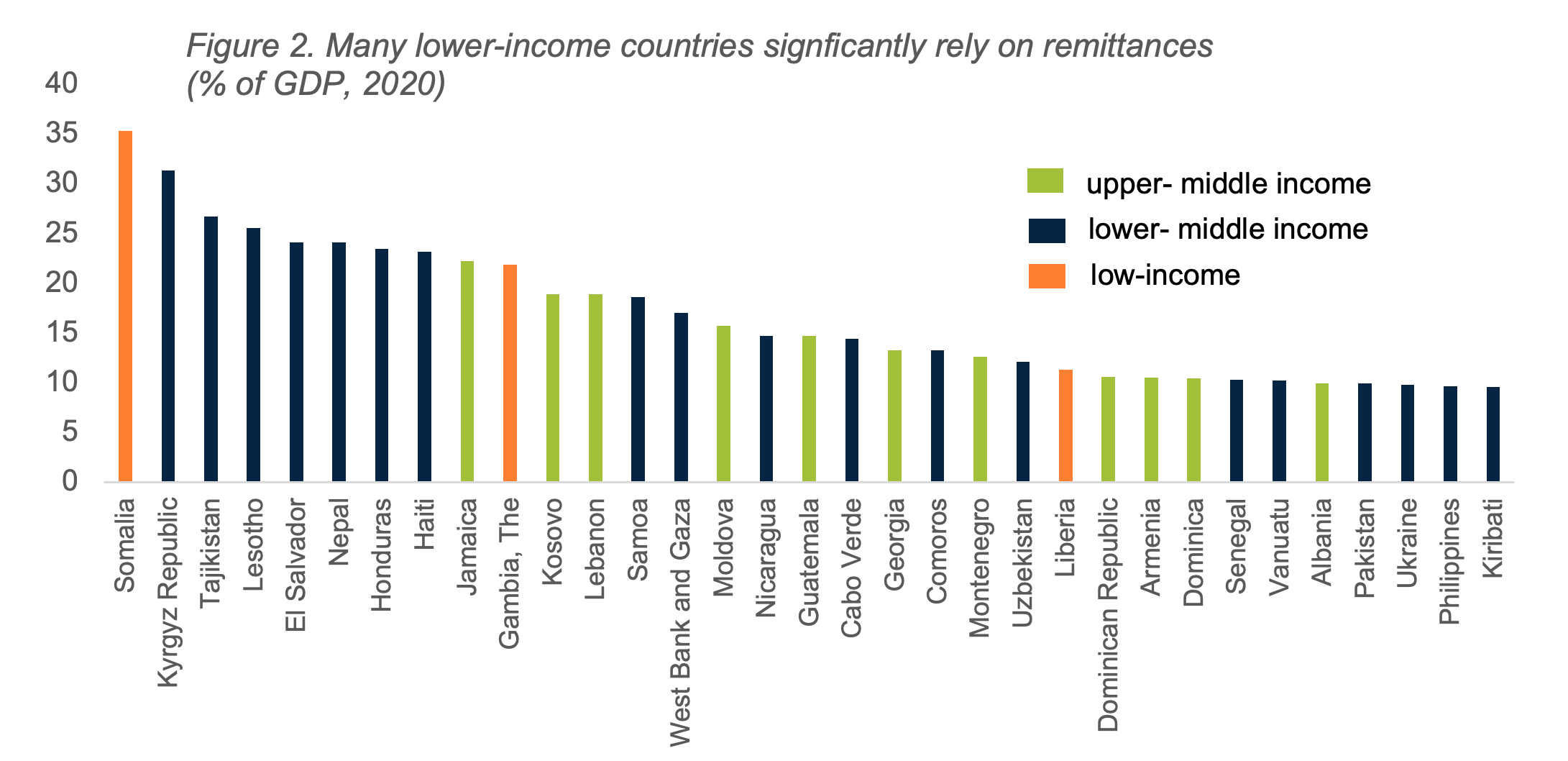

In 33 low- and middle-income countries, remittances were at least 10% of gross domestic product (GDP) in 2020 (see Figure 2 below). They are significantly higher than this in countries including Somalia (35% of GDP), the Kyrgyz Republic (31% of GDP) and Tajikistan (27% of GDP). Moreover, official estimates understate the true size of remittance flows which do not take into account remittances through informal channels.

Source: Based on data from World Bank Development Indicators.

From a household perspective, remittance flows are a significant, stable, and resilient source of income. They also help reduce poverty, increase household investment, improve health and education outcomes, and promote entrepreneurial activity.

Remittances also play a countercyclical role in response to economic shocks. Research shows that migrant workers tend to send more money back during economic downturns in their home countries. This was again evident during the height of the pandemic in 2020, when remittance flows registered a much smaller decline (1.9% below 2019 level) compared to original projections (20% below 2019 level) despite the global nature of the downturn.

They also play a critical role in alleviating some of the economic hardship arising from war. When the conflict in Yemen intensified in 2015, worsening an already dire economic situation, remittances increased from 8% to 12% of GDP in 2016. And in response to the current conflict remittance flows to Ukraine are expected to increase.

What’s the problem?

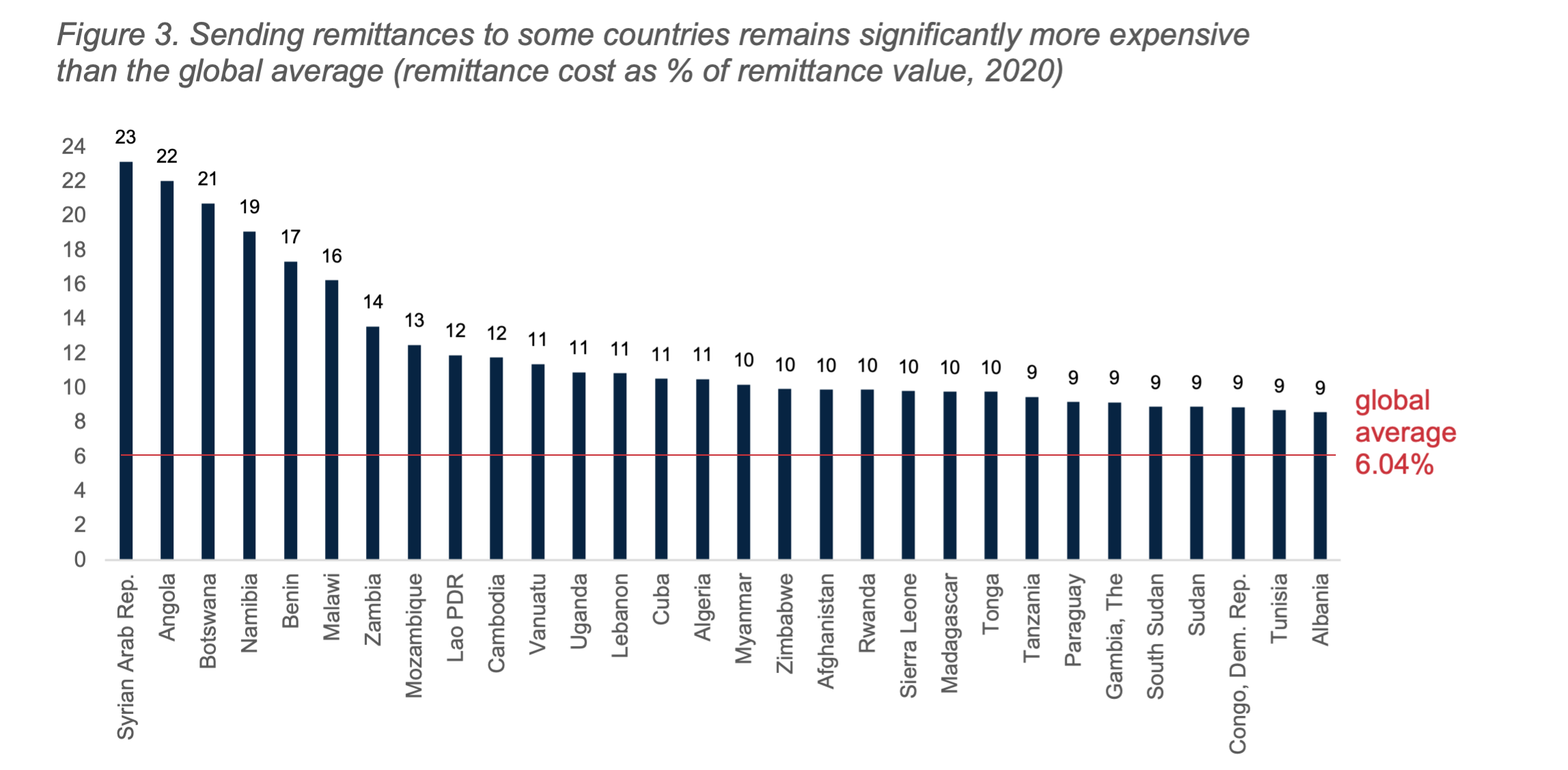

The cost of sending remittances remains too high. Although it is falling, it is not falling fast enough. And it remains far too high for many remittance corridors where informal channels provide lower costs but come with risks.

The sustainable development goals include a target to reduce remittance costs to less than 3% and to eliminate remittance corridors with costs higher than 5% by 2030. Estimates suggest that a 1% reduction in cost leads to a 1.6% increase in remittances to low and middle income countries. While the global average cost of sending $200 has fallen from approximately 10% to approximately 6% over the last decade, the cost can still be as high as 20% to send money to countries including Syrian Arab Republic, Angola and Botswana (Figure 3).

The high cost of formal channels can lead individuals to resort to cheaper informal channels which may also be faster and more accessible because they use a common language, share historical and cultural ties, and do not require identification. However, there are growing concerns that informal remittances are hampering productive financial intermediation, and that their largely undocumented nature makes them prone to illegal activities (e.g., smuggling, money laundering), financial abuse and financing for terrorism.

Source: Based on data from World Bank Development Indicators and World Bank 2021 Remittance Prices Worldwide report.

Unsurprisingly, greater competition among remittance service providers (RSPs) has the most robust association with lowering remittance costs through formal channels, particularly through the entry of financial technology (fintech) companies or digital money transfer operators (MTOs). And recent World Bank data show that sending $200 is most expensive via banks (10.4%), followed by post offices (8.3%) and MTOs (5.2%), and cheapest via mobile operators (3%), while Naghavi and Scharwatt (2018) estimate that sending $200 via mobile money has an average cost of just 1.7%.

This suggests that mobile money may be one of the most effective ways of introducing more competition into the financial sectors of recipient countries, and competing with informal channels which offer costs ranging from 3% to 5%.

Mobile money is defined as ‘a service in which the mobile phone is used to access financial services’ and mobile money transfers occur when there is ‘a movement of value that is made from a mobile wallet, accrues to a mobile wallet, and/or is initiated using a mobile phone’ (GSMA, 2010). Using mobile money for remittances has four advantages:

- it is about 50% cheaper than transfers via MTOs;

- it tends to drive down remittance costs of other RSPs;

- it offers high levels of AML/CFT monitoring capabilities; and

- it allows users and recipients to access other financial services (e.g., savings, e-payments, humanitarian cash transfers).

Despite the advantages, mobile money represents less than 3% of all remittances globally as of 2021. Three factors may explain the low utilisation of mobile money for remittances, especially in low-income countries (LICs) where most of the recipients of remittances reside.

- First, the level of digital readiness is low. The share of population in LICs that have access to electricity is at 42%, mobile cellular subscription at 58%, and internet users at 21% as of 2020.

- Second, there is a lack of financial inclusion. Only a third of the adult population in LICs have an account at a financial institution or with a mobile money service provider as of 2017.

- Third, there are interoperability challenges around the digital payment infrastructure and regulatory frameworks between receiving and sending countries. For instance, as of 2017 there are 126 remittance corridors where mobile money can be used only to receive remittances, but there are only 53 remittance corridors that can be used to both receive and send remittances.

What can be done?

There are various measures that the public and private sectors can take both individually and in partnership with each other to encourage greater use of mobile money for remittances. These include:

- Providing an enabling environment to foster competition by streamlining license application processes for digital RSPs; extending a risk-based regulatory approach between operators of low- and high-value remittance transactions; and supporting partnerships among different RSPs including banks, non-banks, fintech companies, mobile operators, MTOs and postal networks.

- Establishing/expanding physical public infrastructure. Particularly in LICs, prioritise the physical infrastructure for digital transformation including stable access to electricity, mobile networks and internet connectivity.

- Establishing/expanding digital public infrastructure through digital public goods. There is also a need to improve the interoperability of payment and information technology systems among RSPs. Successful digital ID and digital payment platforms can provide the blueprints for other countries to build their own digital public infrastructure.

- Increasing and tailoring fintech/digital remittance literacy programmes based on different characteristics of migrants, diaspora and remittance recipient groups.

- Increasing engagement between public-private sectors and among RSPs especially in response to shocks. The pandemic provided some lessons on successful initiatives which can be leveraged on to mobilise remittances through official and/or digital means, including: providing incentives to use regulated financial services (e.g., Nigeria and Bangladesh); using SIM card registrations for KYC due diligence in opening mobile money accounts (e.g., Egypt and Ghana); public-private sector promotion of digital remittances, such as step-by-step guides on social media; and inter-company collaboration to facilitate remittances via mobile wallets (e.g., MoneyGram and Airtel Africa Money, Paypal and key African markets).