The Indo-Pacific Economic Framework is not a free trade agreement – but how can it lead to tangible growth and developmental impacts for Southeast Asia?

Major economies have been gaining more interest in the Indo-Pacific region. In previous ODI analyses, we covered how the UK’s Indo Pacific strategy can be designed to enhance aid, trade, and investment between the UK and Asian countries. In May 2022, the US launched its Indo-Pacific Economic Framework for Prosperity (IPEF) which, unlike traditional free trade agreements (FTAs), does not offer binding commitments on market access or tariff concessions. Members of the Association of Southeast Asian Nations (ASEAN) are at the center of these Indo-Pacific tilt initiatives, which raises the question: how can they benefit from the IPEF? This analysis argues that the IPEF may provide tangible growth and developmental impacts if the framework can extend technical and financial assistance for digital inclusion; facilitate transformative and diversified investment; and mobilise climate financing for lower-income IPEF partners in ASEAN.

1. The US-led IPEF – the latest addition to the rising global economic and political interest in the Indo-Pacific

The IPEF, launched on 23 May 2022, is one of the latest formalisations of the major economies’ strategic approach towards the Indo-Pacific region. This also signals the revival of the US’ involvement in the region, in the context of the US’ withdrawal from the Trans-Pacific Partnership five years ago. Similarly, China, the EU, and the UK have been increasing their efforts to forge multilateral trade agreements and/or engagements with countries in the region. This is a recognition of the Indo-Pacific’s collective strength as a large market base with a growing middle class with production dynamism and innovation and, perhaps most importantly, as a part of foreign policy around regional security issues.

The Indo-Pacific strategy has been prominent in the UK’s 2021 Integrated Review of Security, Defence, Development and Foreign Policy, as well as the UK’s latest 2022 International Development Strategy. The EU also released a joint communique in April 2021 on its strategy for cooperation in the region. This was stepped up in May 2022 to prioritise inclusive development, green transition, digital connectivity, governance, security and defence, as well as human security. In September 2021, a trilateral security partnership between Australia, the UK, and the US (AUKUS) was launched in order to deepen diplomatic, security and defence cooperation with the Indo-Pacific region as their primary target. To some extent, the non-membership of the US in the Regional Comprehensive Economic Partnership Agreement (RCEP) where China is a dominant player, coupled with the exclusion of China among founding members in US-led IPEF, reflects the strategic importance of the Indo-Pacific in the rivalry between the world’s two biggest economic powers.

2. What is the IPEF (and what is it not?)

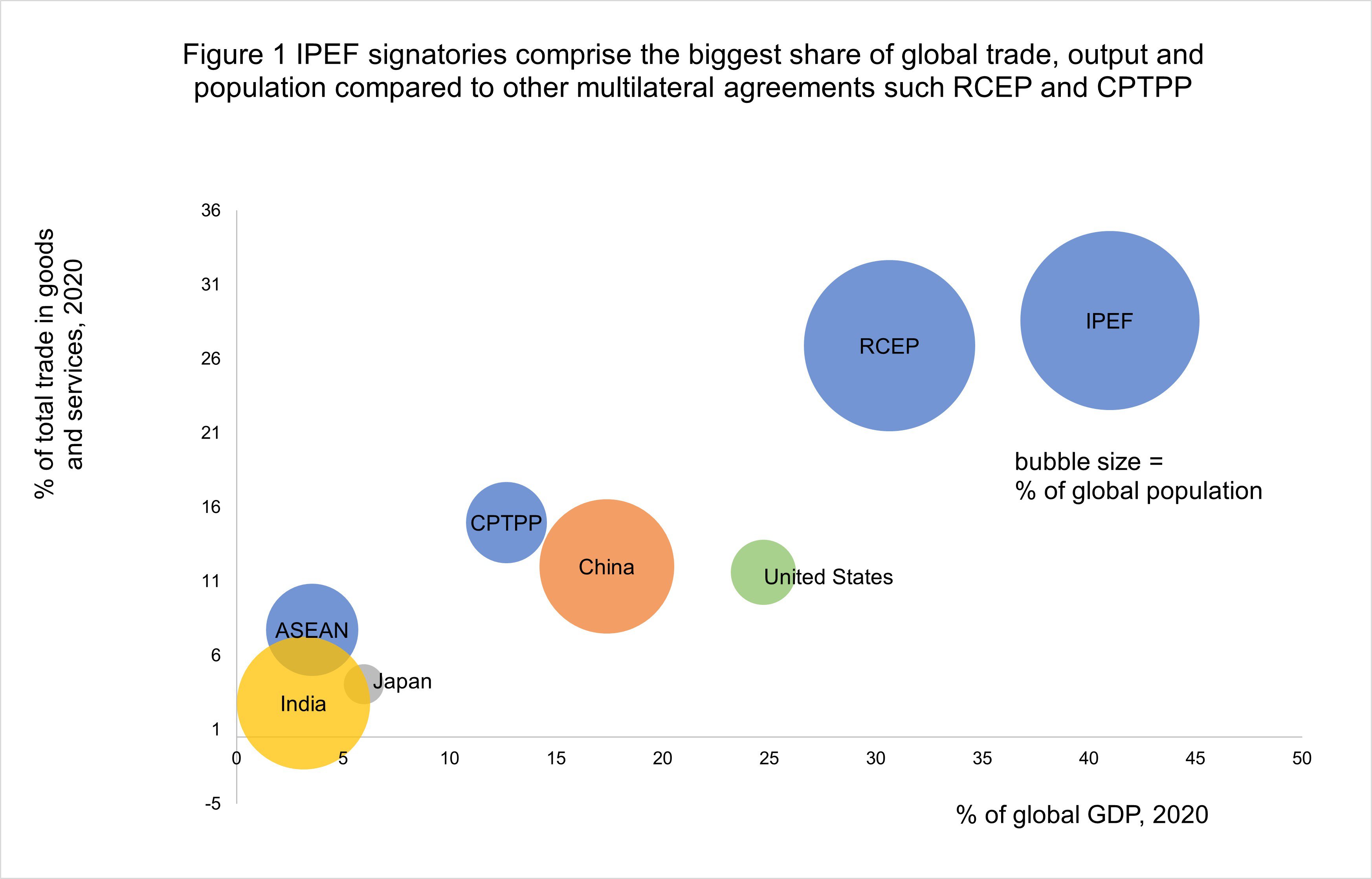

Together, the 14 IPEF founding members comprise a substantial share of global output (41%) and trade (28%) (Figure 1). Unlike other multilateral FTAs with binding commitments to reduce trade tariffs such as RCEP or the CPTPP, the IPEF is not an FTA. The launched IPEF has no iterations on market access or tariff reductions among member states. Instead, the IPEF is an ‘economic arrangement designed to tackle 21st century challenges’ by establishing “high-standard commitments” around four main pillars. These include trade (largely on the digital economy); supply chain resilience; clean energy, decarbonization and infrastructure; and tax and anti-corruption. The IPEF aims to have signed agreements once commitments have been negotiated. However, there is little information around specifically what form these commitments will take (e.g., economic policies, financial assistance), whether agreements will be binding or not, and which countries will formally commit to which pillars. By identifying these priority areas and limitations in the current form of this US-led IPEF, it is possible to identify entry points where IPEF partners (especially lower-income signatories) can benefit the most (more in section 4).

Figure 1 IPEF signatories comprise the biggest share of global trade, output and population compared to other multilateral agreements, like RCEP and CPTPP

Source: Author’s computations using data from World Development Indicators

3. Southeast Asia is in the middle of Indo-Pacific agreements – so how can they benefit from the IPEF?

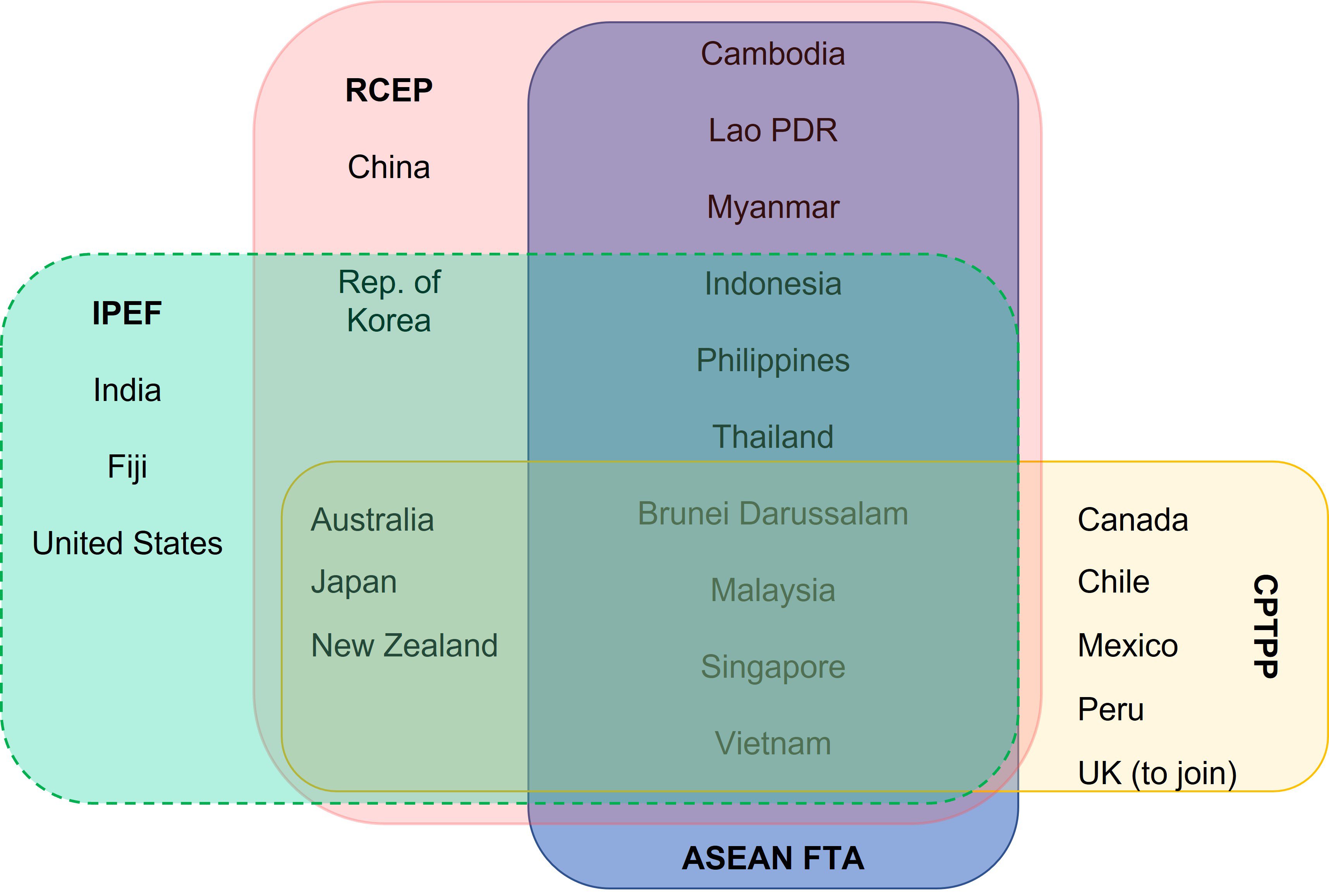

While the IPEF could be potentially beneficial to its 14 members, it may also help bolster and transform growth in ASEAN. Firstly, this is due to the fact that the majority of ASEAN signatories to this framework (i.e., Malaysia, Thailand, Indonesia, Philippines and Vietnam) have a lower income per capita (with the exception of India) than the other high-income countries that are already members of the IPEF. For instance, Vietnam has a per capita of $2,786. This is significantly lower than the average IPEF members’ per capita ($13,840) and far behind that of the US ($63,207) as of 2020. Secondly, ASEAN is at the center of Indo-Pacific strategies and agreements (Figure 2). This strategically positions ASEAN members in the IPEF to become channels supporting positive spillover effects to other non-IPEF ASEAN members at lower levels of economic development (i.e., Cambodia, Lao PDR and Myanmar). This will likely result in increased synergy from complementary, multilateral initiatives.

Figure 2 ASEAN countries are at the center of multilateral cooperation in the region

Source: Author's compilation

4. How can the IPEF work for lower-middle income ASEAN members?

While the IPEF has yet to obtain any binding commitments, increased cooperation and developmental support can lead to tangible results for lower-income ASEAN members. That being said, this can only be done if the IPEF can spearhead the following: technical assistance to expand digital inclusion, facilitation of transformative and diversified investment, and mobilisation of official and private climate finance.

a) Extend technical assistance from IPEF members with advanced digital ecosystems to expand digital inclusion in ASEAN

Digital inclusion is necessary for the e-commerce sector’s business to business (B2B) and business to customers (B2C) transactions at the domestic, regional, and international levels. These are integral if the IPEF aims to augment a mutually beneficial and inclusive digital economy among IPEF members (first IPEF pillar.) In ASEAN, digital trade is significant, however digital inclusion remains a challenge. For instance, the share of ICT exports in relation to total goods exports in Vietnam has increased from an 8% share in 2010 to a 39% share in 2020. Additionally, digitally deliverable services are thriving, reaching 50% to 75% of total trade in services in Indonesia, Malaysia, Singapore and the Philippines, as of 2020. However, the share of businesses that use the internet to deliver products online was 50% in the Philippines, and only 11% in Indonesia, as of 2015. Within Indonesia, this ratio is only 2.5% of micro enterprises and 10% of small enterprises.

Through the IPEF, ASEAN partners can seek technical assistance (with limited financial assistance) from IPEF partners with advanced digital ecosystems around expanding digital usage among individuals, businesses and governments (e.g., support to improve digital skills and infrastructure). They are also able to receive guidance around how to effectively govern their network economies. Examples of such initiatives can be found in Australia’s technical support in developing the Cambodian government’s national digital strategy in the context of Covid-19. This can be extended to digitising government transactions, which can be leveraged to increase tax compliance, improve transparency of procurement and audit agencies, and reduce red tape – consistent with the IPEF’s pillar on tax effectiveness and anti-corruption

b) The IPEF can facilitate expansion and promote diversification of US FDI in the ASEAN region

The IPEF aims to seek supply chain commitments to preserve price stability using coordinated diversification efforts to achieve this. On the trade front, around a third of the US’s imported goods from this region are electronics and machinery according to 2020 WITS data. This has served to reinforce the trade of value-adding products that are conducive to the transformation of the ASEAN economy.

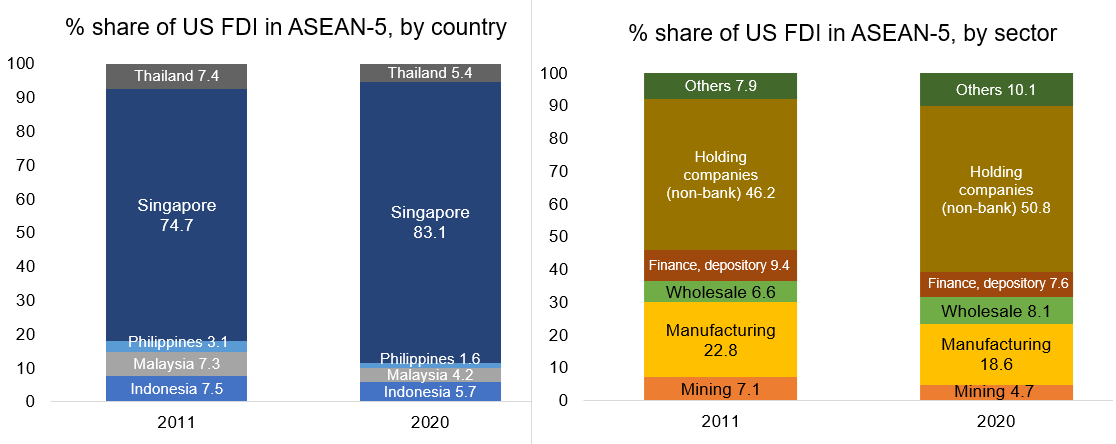

However, there is room to expand and diversify the US’ foreign direct investment (FDI) in the region. One such avenue could be through enhancement of investment facilitation and promotion among members of the IPEF. FDI drive expansion and integration of global value chains (GVCs). In turn, GVCs with diversified and geographically dispersed suppliers can be a source of resilience in times of shocks, based on World Bank and IMF analyses. Currently, the US’ FDI in ASEAN is concentrated in Singapore, comprising 83% of the US FDI in the region, as of 2020 (Figure 3). By sector, the US’ FDI is largely concentrated in holding companies in Singapore (Figure 3). In Indonesia, three quarters of US FDI is concentrated in mining activities, as of 2020—prompting discussion on how the US can expand its role in supporting ASEAN’s resilience through transformative FDI across the region.

Figure 3 US FDI has been concentrated in Singapore – the IPEF should aim to redistribute transformative investment across ASEAN members

Source: Author’s computations based on data from US Bureau of Economic Analysis

c) The IPEF can help mobilise official and private climate finance

The IPEF’s third and fourth pillars are focused on promoting a clean and fair economy. It aims to accelerate multilateral efforts among partners to tackle the climate crisis. Bilaterally, the US committed a $40 million investment aimed at mobilising roughly $2 billion of blended finance for clean energy and infrastructure in ASEAN. This is relevant for the region, since 5 out of 10 ASEAN members reside in the top 20 countries that have been most affected by climate change between 2000 to 2019—Myanmar (2nd), Philippines (4th), Thailand (9th), Vietnam (13th) and Cambodia (14th). The ISEAS-Yusof Ishak Institute estimates that only 10.6% ($56 billion) of the total climate finance mobilised for developing countries between 2000 and 2019 went to ASEAN (with the exception of Brunei and Singapore). Yet, the Asian Development Bank estimates that ASEAN members need $210 billion annually up to 2030 to adequately finance investment in climate-compatible infrastructure. This is a substantial financing gap, which creates an opportunity for the IPEF to play a direct (e.g., through financial and technical assistance) or indirect supporting role (e.g., mobilising private finance).

There are a plethora of questions that warrants close monitoring as the IPEF negotiations progress, namelythe levels of reciprocity and whether commitments will be binding to help ensure the durability of the framework beyond the incumbent administrations. Additionally, these negotiations provide windows of opportunity for IPEF members to pursue meaningful cooperation around digital inclusion, transformative and diversified FDI, and climate finance. These are likely to help bolster ASEAN’s income and resilience against future shocks.