In this instalment of Budgets and Bytes we are checking in on recent developments in digital money, their potential benefits for lower income countries, the role of government in their adoption, as well as some worrying and interesting developments in El Salvador and The Bahamas respectively.

The benefits of digital payments

As well as the benefits for improving the efficiency, transparency, and accountability of government operations, there are wider benefits to transitioning from cash to digital payments.

"A range of studies have demonstrated that moving from cash to digital payments can boost productivity and economic growth, improve transparency, increase tax revenues, expand financial inclusion, and open up new economic opportunities, particularly for women and disadvantaged communities."

For lower income countries that lack traditional banking infrastructure and are highly dependant on remittances, the benefits may be even greater.

The role of government in accelerating the transition to digital payments

As one of the largest payers and payees in an economy, governments have enormous influence over which payment methods become mainstream. Digitizing government payments and receipts are among 10 policy options identified by the Better Than Cash Alliance for accelerating the transition to digital payments.

Table 1. Payment Grid: Types of Payments by Payer and Payee

| Payer | Payee: Government | Payee: Business | Payee: Person |

|---|---|---|---|

| Government | G2G - Budgetary allocations, funding | G2B - Grants, payments for goods and services | G2P - Welfare programs, salaries, pensions |

| Business | B2G - Taxes, fees for licenses | B2B - Payments for goods and services | B2P - Salaries and benefits |

| Person | P2G - Taxes, utilities | P2B - Purchases | P2P - Remittances, gifts |

Most have moved, or are moving, towards digital payments as a way of reducing the costs and curbing the corruption associated with cash payments. These range from electronic fund transfers (EFT) for managing public payrolls and payments to suppliers, to more innovative G2P e-money payments to target cash transfers for hard-to-reach populations through mobile phone network operators in lower income countries. Some are even facilitating P2G e-money payments for government services. See Table 1 for different types of government payments and receipts.

Government adoption of digital payments can thus support a virtuous circle by encouraging more widespread use leading to greater financial inclusion and the associated benefits.

Nevertheless, for many poor countries, financial inclusion remains stubbornly low, and the cost of sending remittance payments remains stubbornly high.

The latest advances in digital money and payments offer new promises as well as risks

Newer forms of digital money are now emerging that purport to make financial inclusion and lower remittance costs more realisable.

These are generally grouped into three categories: central bank digital currencies (CBDCs); stablecoins; and cryptocurrencies (see list below), though there are various nuances to each – see here for a more detailed discussion.

- CBDCs: Issued by the public sector. Essentially a digital version of cash that can be stored and transferred using an internet or mobile application. The Bahamas Sand Dollar is the only one currently in use (see section below). China has a CBDC in trial phase.

- Stablecoins*: Issued by the private sector. Redeemable at fixed value. Backed by safe and liquid assets. A type of e-money like AliPay, We Chat Pay, and M-Pesa, but distinguishable by its use of decentralised rather than centralised payment settlement technology. Examples include Paxos, USD-Coin, and True USD.

- Cryptocurrencies: Denominated in its own unit of account, it is created (or “minted”) by nonbanks, and is issued on a blockchain, commonly of the permissionless type. The most well known and widely used is Bitcoin. Most financial institutions view them as speculative assets rather than digital money, and use the term ‘crypto asset’ rather than the more popularised ‘cryptocurrency’ to describe them.

CBDCs are essentially a government response to the rise of other forms of digital money and the associated risks. Cryptocurrency trading has been described as the new ‘wild west’. China has recently clamped down on cryptocurrencies and is trialling its own CBDC. Bitcoin has also been heavily criticised for its role in financing illegal activities and its negative environmental impact. The latter is due to the amount of electricity consumption required in Bitcoin mining operations, which has been estimated to be same as the electricity consumption of Switzerland.

“By now, it is clear that cryptocurrencies are speculative assets rather than money, and in many cases are used to facilitate money laundering, ransomware attacks and other financial crimes. Bitcoin in particular has few redeeming public interest attributes when also considering its wasteful energy footprint.”

Most countries are taking a cautious approach. For example setting up taskforces to weigh up the benefits and risks associated with CBDCs, while looking into ways to regulate new forms of digital money and their providers.

Nevertheless, one country, The Bahamas, has already introduced a CBDC (see below). Meanwhile another, El Salvador, recently took the more controversial decision to make Bitcoin legal tender (see next). Other policy makers are beginning to view e-money, like stablecoins, as offering a bridge to a ‘synthetic’ CBDC (see below).

El Salvador’s decision to adopt Bitcoin as legal tender

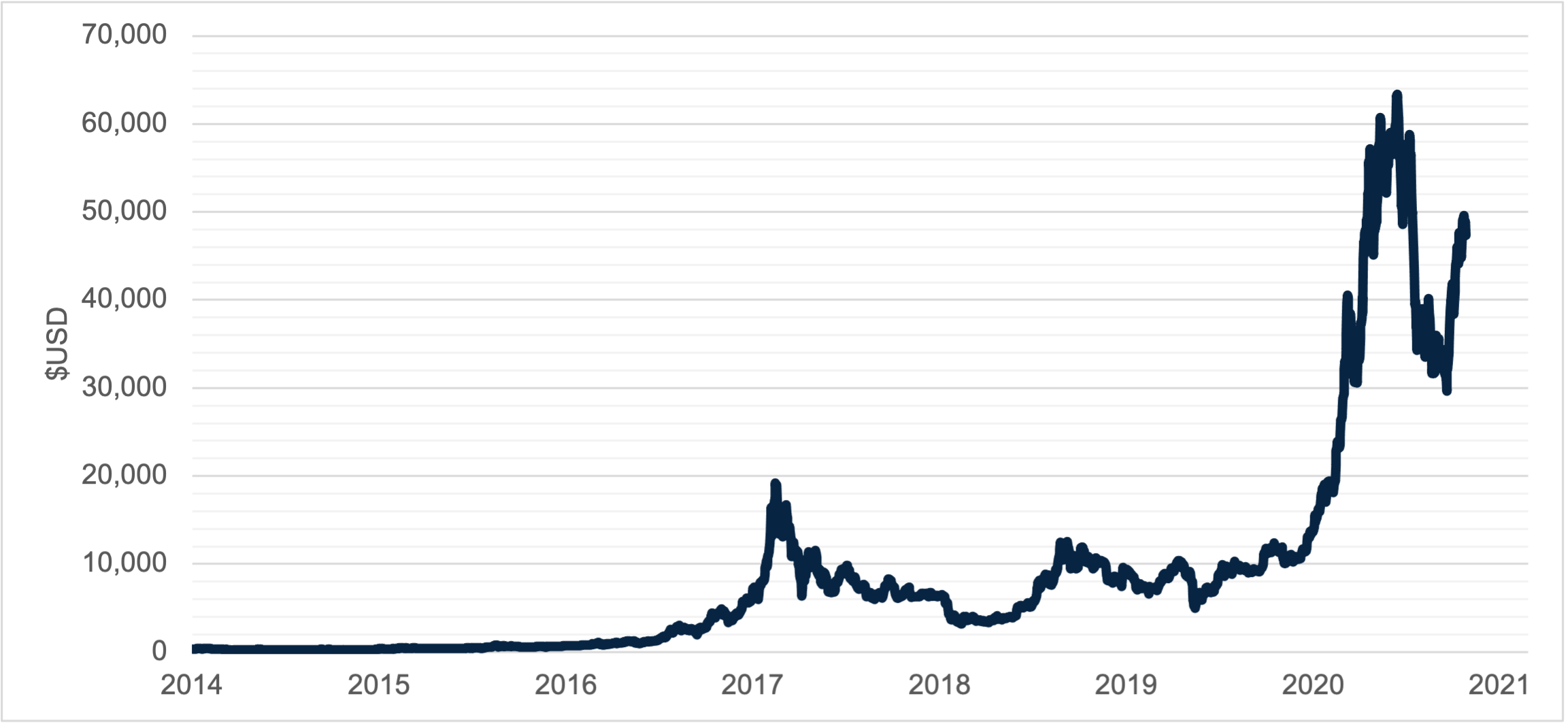

As well as its association with illegality and environmental harm, Bitcoin’s detractors point to the fact that, although it has been around since 2009, it plays ‘almost no role in normal economic activity’. The volatility of its price has also led most to the conclusion that it is not suitable for use or classification as digital money.

Figure 1: Bitcoin daily closing price

Back in February 2019 Martin Wolf of the Financial Times wrote that “the best way to view cryptocurrencies is as speculative tokens of no intrinsic value” while also noting that “one could have value if it became the currency of choice of a jurisdiction”. El Salvador is proposing to put this to the test.

On the 9th of June congress approved a proposal from President Nayib Bukele for El Salvador to become the first country to make Bitcoin legal tender. That initiated a 90-day countdown to the moment when it will be notionally possible for El Salvadorans to pay for goods and services, and even their pay their taxes, using the cryptocurrency.

The two big benefits El Salvador is chasing are:

- Lower international financial transfer costs – remittances accounted for 24% of El Salvador’s GDP in 2020 at an average transaction cost of 2.85%.

- Greater financial inclusion – just 30% of the population aged 15 or over had an account with a financial institution or mobile money service provider in 2017.

President Bukele is also hoping the move will encourage more investment, tourism, innovation and economic development. He has even floated the idea of offering bitcoin mining facilities using renewable energy from the country's volcanoes, perhaps in response to China’s recent clampdown, and growing anti-cryptocurrency sentiment in the US from everyone from Elon Musk to Elizabeth Warren.

El Salvador’s decision has been met with scepticism and worry

In Washington D.C. the IMF and World Bank were apparently unimpressed. Reuters reported that the move is putting a potential $1 billion economic recovery program with the IMF in jeopardy. The IMF itself has been coy, preferring to reiterate a more general stance that: ‘adoption of bitcoin as legal tender raises a number of macroeconomic, financial and legal issues that require very careful analysis’ in its press briefings.

And the World Bank turned down a request for assistance on the implementation of the law citing concerns over transparency and the environmental impact of Bitcoin mining.

"The passing of Bukele’s Bitcoin Law has been met with scepticism and worry by essentially every financial institution on the planet, starting with the World Bank and the International Monetary Fund."

The Financial Times reported that:

- A survey by the El Salvador Chamber of Commerce and Industry found that “90 per cent of respondents did not want to be obliged to accept bitcoin as payment and three-quarters vowed to continue using dollars”, and

- “A poll by the Universidad Francisco Gavidia found 44 per cent expected it to make the economy worse”.

The credit rating agency, Fitch, has warned that it “will likely be a credit negative for local insurance companies” due to “higher FX and earnings volatility risk as well as additional regulatory and operating risk considerations”.

For a finance ministry, the prospect of receiving revenues in a currency that has previously declined by as much 20% in one day is a major cause for concern.

Of course, the whole thing could be just a lot of noise. Like a more traditional financial system, cryptocurrencies require infrastructure, most notably internet access and smartphones (but also machines for exchanging cryptocurrencies with dollars, of which not many are currently in place). In 2017 just 34% of the population of El Salvador used the internet. There has also been some rowing back of the legal mandate to accept Bitcoin as payment in recent days.

While not naming El Salvador, a recent blog post by IMF staff, has called the move “a step too far” and “an inadvisable shortcut” towards realising the benefits of digital money.

The Bahamas becomes the first country to introduce a CBDC

While the international financial institutions are cold on cryptocurrencies, they seem to be warming up to the idea of central bank digital currencies (CBDCs).

The June issue of the IMF’s Finance & Development magazine includes an article weighing up the benefits and risks of CBDCs and other forms of digital money, and arguing that “digital money has the potential to transform the financial sector, and that emerging markets and lower-income countries stand to gain the most from this dramatic shift”. These are similar points to those made by ODI’s Chief Executive Sara Pantuliano to the World Economic Forum in February.

Unlike Bitcoin and other cryptocurrencies, which experience wide daily fluctuations in their price, CBDCs are pegged 1:1 to a country’s own currency – essentially digital cash.

The Bahamas became the first country in the world to issue a CBDC in October last year. As in El Salvador, the aim is to increase financial inclusion in a country where it is “unprofitable for commercial banks to have ATMs or physical branches on remote, sparsely populated islands” and “extreme weather events make the cost of maintaining infrastructure even steeper”.

However, the problem of transaction fees on international transfers from abroad remains. While this may be addressed as more countries issue CBDCs, a recent joint report by the World Bank, IMF and Bank for International Settlements suggests there are many miles to go before this is realised.

As detailed in the Bank for International Settlements latest annual economic report there are various ways in which a CBDC could operate, requiring careful risk analysis, and multiple policy decisions. And if they are to bring down the cost of cross border payments such as remittances, they will likely require international cooperation to allow sharing of digital identification across borders.

Stablecoins might be a bridge towards CBDCs

Stablecoins may offer a potentially better and less risky path to realising the benefits of digital money than cryptocurrencies while the world waits for CBDCs to become more ubiquitous.

They could also end up being a key part of the CBDC architecture. Although one of the design choices is for central banks to create and operate their own CBDCs, it seems likely that they will engage the private sector to do the heavy lifting with respect to consumer facing activities. Indeed, this is the approach The Bahamas has taken in the example discussed above.

"A logical step in [the design of CBDCs] is to delegate the majority of operational tasks and consumer-facing activities to commercial banks and non-bank PSPs [payment service providers] that provide retail services on a competitive level playing field. Meanwhile, the central bank can focus on operating the core of the system."

From this perspective, treating e-money providers (such as those that issue stablecoins) more like commercial banks (by allowing them access to central bank reserves and the regulation that comes with that) is a “sleight-of-hand” that could yield a “synthetic CBDC” that also mitigates the risks associated with e-money. These risks are becoming more worrying. For example Stablecoins, such as Tether and USD Coin, are already causing concern for regulators, because it is not clear how well backed they are.

"Synthetic CDBC outsources several steps to the private sector: technology choices, customer management, customer screening and monitoring including for “Know Your Customer” and AML/CFT (Anti-Money Laundering and Combating the Financing of Terrorism) purposes, regulatory compliance, and data management — all sources of substantial costs and risks. The central bank merely remains responsible for settlement between trust accounts, and for regulation and close supervision including eMoney issuance. If done appropriately, it would never need to lend to eMoney providers, as their liabilities would be fully covered by reserves."

But risks remain, especially when cross border payments are added to the mix. From the perspective of a lower income country dependent on remittances this is one of the most desirable features of e-Money. But it could also spell the end of weak currencies by accelerating the path to dollarisation and the resulting loss of monetary policy effectiveness.

What happens next?

Increasing financial inclusion and reducing the cost of cross border remittances are likely to remain a high priority for governments in lower income countries. What governments use and accept as payment has enormous influence on what becomes mainstream in the wider economy, so it is therefore important that they choose wisely.

CBDCs could promote greater financial inclusion in lower income countries, but they are unlikely to address the high transaction costs on cross border payments unless they are joined up to a wider international architecture. That architecture appears to be only slowly emerging as central banks figure out the best way to design CBDCs and regulate the cryptoasset markets.

This comes with the significant risk of sweeping away weaker currencies in its wake. However, this may be a risk worth taking compared to reliance on cryptocurrencies as legal tender.

Beginning on September 7th the El Salvador experiment begins. As reported by Reuters, “Central American countries are eagerly waiting to see if El Salvador's adoption of bitcoin as parallel legal tender cuts the cost of remittances, an important source of income for millions of people”.