Ilmi Granoff, Sarah Wykes, Alison Doig, Sam Pickard, Laurie Van Der Burg and Ryan Hogarth

Poverty is the state of human deprivation – deprivation of basic material needs, rights and freedoms, social and political power, education and economic participation. In 2012, almost 900 million people lived on less than $1.90 per day, a level of income considered to be inadequate for basic food, shelter and clothing, and a crude but practical indicator of extreme poverty.

The coal industry asserts that continued investment in coal is needed to grow developing economies and combat poverty. The logic runs that coal is necessary to provide the energy required for industrialisation, the process of structural change from an agrarian society to one based primarily on manufacturing. Historically, industrialisation has enabled some countries to rapidly increase economic productivity, employment and income levels.

The consumption of coal and other fossil fuels for industrialisation, however, is a major cause of global warming. A shift away from coal is necessary for climate protection.

The argument that further expansion in coal energy is needed to combat poverty is based on tenuous assumptions about the relationships between energy, industrialisation and poverty. The following FAQs show why.

Frequently asked questions

Isn’t coal needed to combat poverty?

The logic that coal is needed to combat poverty is based on two premises. The first is that coal provides poor households with electricity. The limitations of coal-fired power as a solution to energy poverty are explored in a previous set of FAQs. The second is that coal is required to power economic growth, which is needed, in turn, to increase poor people’s incomes. Both these premises warrant further scrutiny.

It is true that energy is needed for economic growth. Most economic production – be it agriculture, extractive industries, manufacturing or services – requires an affordable and reliable energy supply. It is a leap, however, to assume that coal should be the energy source of choice for expanded production in any sector.

The amount and type of energy required depends on the form of economic activity it serves. As discussed in the following question, there are alternatives to coal for power generation that are less polluting and, in many cases, cost-competitive.

It is also true that economic growth is needed to fight poverty. Increased economic production can create jobs that enable poor people to work their way out of poverty. It can also generate increased public revenue for spending on pro-poor services such as education, health care, employment programmes and cash transfers.

However, the relationship between economic growth and poverty is complex. While there have been no instances of sustained poverty reduction without economic growth, the figure below indicates that some countries have done a better job at reducing poverty with moderate growth, while others have seen rapid growth with little effect on poverty.

Therefore just as the energy needs of economic growth are sector specific, so too are growth’s poverty impacts. The most energy-intensive models of growth generally do not lead to the most poverty reduction.

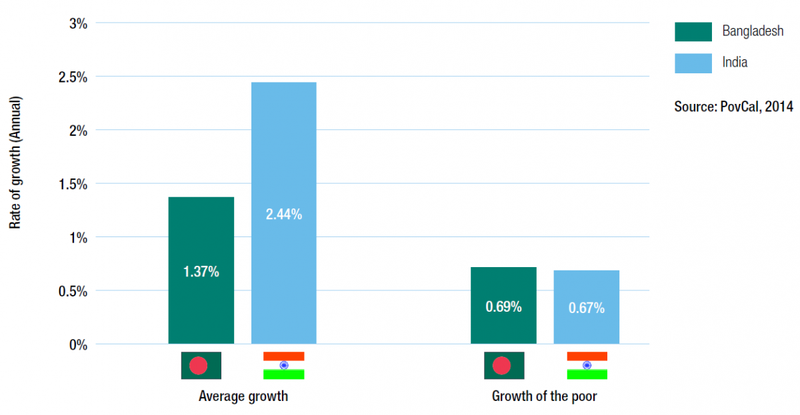

Figure: Comparison of India and Bangladesh

The recent average economic growth rates in India and Bangladesh relative to the average growth in consumption of the extreme poor (those living on less than $1.25 per day). India’s recent growth rate has been 3.6 times higher than that of Bangladesh. However, the two countries’ progress on poverty reduction has been roughly equal – the reason being that poor people in Bangladesh have gained a much larger share of the growth than poor people in India.

Frequently asked questions

Don’t we need coal to power economic growth?

Four-fifths of coal produced globally is used for centralised electricity-generation, an enabling factor in many – but not all – types of economic production. Coal-generated electricity is relatively cheap, but it is also highly polluting.

Power sector planning is rarely driven by the relative costs of different energy sources alone. Nevertheless, there are numerous substitutes for coal power that are increasingly cost-competitive and less damaging to local environments and human health (see figure below). There is an affordable energy alternative to coal in most places, though which option is most attractive varies by location.

Rapid declines in the average cost of electricity from gas and renewables have weakened coal’s competitiveness throughout much of the world. From the US to South Africa to India, unsubsidised wind and solar power is now cost-competitive against conventional coal-fired power plants and cheaper than advanced ‘high efficiency low emissions’ coal technologies. As wind and solar technologies continue to scale, their costs are projected to keep falling. Meanwhile, the cost of coal power has slightly increased, and will increase further as governments introduce more stringent pollution norms.

The shift away from coal is likely to accelerate as renewables gain a greater share of the electricity mix. Once a wind or solar project is built, the marginal cost of generating electricity is near zero, allowing them to outcompete coal power in electricity markets. With renewable energy meeting a greater share of demand, coal plants are increasingly left dormant on windy or sunny days – a factor that has diminished the business case for investment in new coal capacity.

Developing renewable energy instead of coal would more likely boost economic growth than hinder it. The International Renewable Energy Agency (IRENA) found that doubling renewables’ share of global energy mix by 2030 would increase global GDP by up to 1.1% or $1.3 trillion, relative to a business-as-usual scenario based on existing country plans. Production of fossil fuels would decline, but be offset by increased production in the manufacturing, construction, basic metals, silicon and service sectors.

Figure: Global range of electricity generation costs from different sources, 2014/15

The cost of generating electricity varies by place, source and technology. This figure shows the global range of electricity costs across different technologies in US dollars per kilowatt-hour. In specific cases, electricity has been generated from large and small hydro, onshore wind, biomass, geothermal, solar PV and offshore wind at a cost competitive level to coal.

Frequently asked questions

Are there alternatives to coal for other needs besides power?

Approximately 17% of global coal demand is for coking coal, which is used in steelmaking. In contrast to coal for power generation, there are few opportunities to completely substitute coking coal in the process of turning iron ore into steel using blast furnaces.

However, according to new research, the quantity of coking coal can be reduced through the integration of other fuels – natural gas, charcoal and biomass. By integrating biofuels into the steelmaking process, carbon dioxide emissions can be reduced by more than 50%, while keeping the steel industry profitable.

It is also possible to reduce the need for primary steelmaking. Scrap steel can be recycled in furnaces that use three-quarters less energy. Rather than coking coal, these furnaces use electricity, which can be generated by alternative energy sources. Steel can be utilised more efficiently too. Research has shown that commercial buildings in the UK could use up to 46% less steel without compromising their safety. From auto manufacturing to construction, alternative materials to steel could also be used.

Heat for cement making also currently relies heavily on coal, but can be produced by alternative energy sources like natural gas and biomass, despite coal industry claims. The bigger challenge for cement is limiting pollution from chemical reactions during production, not energy. Like steel, new alternative materials offer promising opportunities to replace cement altogether, along with the energy it consumes.

Frequently asked questions

Can renewables meet rising demand for electricity?

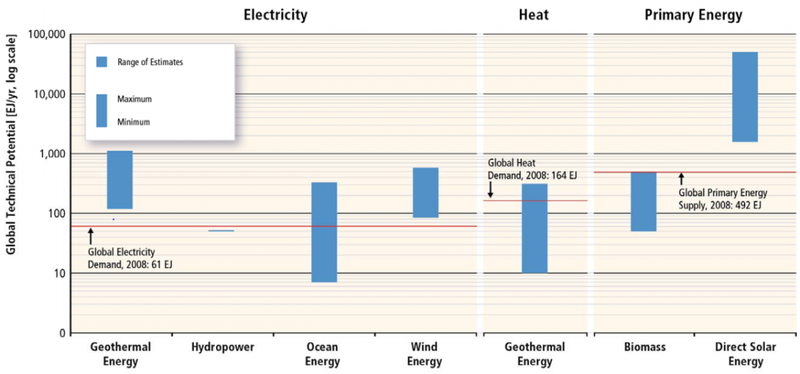

The potential supply of renewable energy using existing technologies is many times greater than current energy consumption. As seen in the figure below, solar, wind, biomass, geothermal and ocean energy is so abundant that each source could potentially supply the entire world’s electricity demand.

Global resource maps clearly show that both developed and developing countries are endowed with substantial renewable resources. A recent African Development Bank report found that ’Africa’s reserves of renewable energy resources are the highest in the world.’

Renewables already dominate many electricity grids. In 2012, over 50 countries produced more than half their electricity from renewables. Most existing renewable capacity is hydro, because this was the first form to be competitive with fossil fuels. However, a number of countries have installed significant shares of non-hydro renewables, including Guatemala, Kenya and Denmark.

Despite their potential, renewables currently generate just 22% of global supply. This small share, however, is a poor indicator of current trends. Power stations are long-lived assets, and our current electricity mix is a hangover from the fossil-fuelled power plants installed decades ago. A more useful metric to understand trends is to look at the kind of power stations being planned and commissioned now.

It is clear that renewable energy sources will provide an increasing share of global electricity in the coming decades. Even under the International Energy Agency’s (IEA), overly conservative renewable energy forecasts, the wind and solar PV generating capacity built over the next 25 years will amount to double the coal capacity added under business-as-usual policies. According to IEA, it is likely that the amount of non-hydro renewable generating capacity built between 2014 and 2020 will outweigh that from all fossil fuels. With the rapidly declining costs of solar power, solar capacity additions are likely to surpass IEA forecasts.

Figure: The technical potential for renewable energy sources to meet global energy demands

Ranges of global technical potentials of renewable energy sources. Biomass and solar are shown as primary energy due to their multiple uses; note that the figure is presented in logarithmic scale due to the wide range of assessed data. Technical potential is the total amount of energy that could be obtained using demonstrated technologies or practices.

Frequently asked questions

Isn’t coal power necessary for a reliable electricity system?

Developing countries often have extremely unreliable electricity systems, prompting some to argue that new coal power stations are needed to supply more power. In many cases, this justification is misguided. Many unreliable electricity systems do need more supply but, as discussed earlier, there are generally better options than coal for filling the supply gap.

In other cases, adding more generating capacity – coal or otherwise – will not improve the reliability of an electricity system.

India for example, added more capacity in 2014/15 than any other year on record, yet continued to suffer chronic blackouts. The blackouts were as frequently due to distribution companies imposing them to manage demand from non-paying consumers as to supply shortages – more than a third of coal capacity went unused in 2014/15.

Another common misconception is that because ’intermittent’ energy sources like wind and solar only generate electricity on windy or sunny days, they must be supplemented by a ‘baseload’ energy supply like coal that can provide power all of the time.

Most countries do not yet have enough wind and solar in their electricity mix to have to worry about the intermittency of supply. As the share of renewable energy capacity grows, there are many options to balance mismatches between supply and demand. Hydropower, pumped storage, geothermal, nuclear and natural gas plants generally offer more responsive options than coal. They can be turned off and on at any time to back up renewables like wind and solar (though large hydro, nuclear and natural gas also have environmental impacts that must be considered).

Eventually, the need for responsive electricity generating options will be negated by:

- ‘demand response’, technologies and practices that shift the timing of electricity consumption to when supply is greatest

- interconnected grids that move electricity from one place to another as needed

- energy storage technologies, which are already on the cusp of competitiveness.

Frequently asked questions

Wasn’t coal-driven industrialisation the cause of East Asia’s recent success in reducing poverty?

East Asian countries, China, Japan, South Korea, Taiwan and Vietnam, recently went through a period of rapid industrialisation. A large supply of affordable energy from coal enabled them to grow rapidly by powering their manufacturing sectors. This industrialisation was a factor in reducing urban poverty and sustaining poverty reduction. However, the relative contribution of industrial growth (and the related expansion of coal power) to the overall gains on East Asia’s poverty is often overstated.

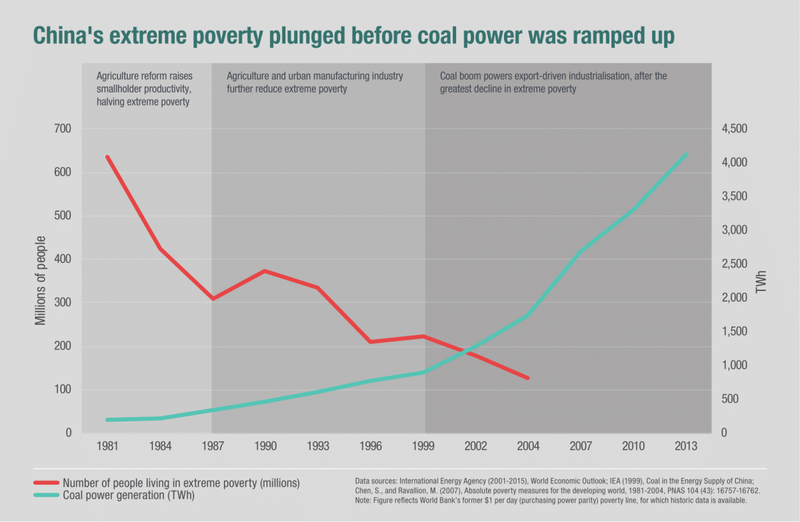

Take China: between 1981 and 2004, the number of people living on less than $1 per day declined by 500 million. China’s industrial sector grew an unprecedented 12% per annum from 1985 to 2005. From 1987 onwards, newly added coal capacity in China dwarfed that of any other country and was largely geared towards powering industrial growth.

However, research by World Bank economist Martin Ravallion shows that two-thirds of the decline in households living in extreme poverty occurred between 1981 and 1987, prior to the boom in industrial growth and the large-scale expansion in coal power (see figure below).

Urbanisation, combined with growth in export-orientated manufacturing, can be credited with less than one-quarter of the poverty reduction between 1981 and 2004. Instead, the driving force behind China’s success in reducing extreme poverty was growth in agricultural productivity, enabled by regulatory changes that dismantled collective farms and empowered smallholder farmers to benefit economically from managing their own farms. Between 1980 and 1985, agricultural productivity increased on average 7.5% per year, much of which accrued to the poorest households.

Small-scale agriculture remains the primary employer in the majority of least developed countries. In sub-Saharan Africa, it employs seven times as many people as industry. Agriculture also requires energy, but smallholders’ energy needs are often served most cheaply by distributed technologies like internal combustion engines and off-grid or mini-grid electricity connections powered, in many cases, by renewable technologies such solar PV, wind and hydro.

Frequently asked questions

If China were to begin industrialising today, would it opt for coal?

China’s experience of coal-powered industrialisation and rapid economic growth is often used as evidence that other countries wanting to pursue a similar industrialisation pathway will also need coal. But the decisions that drove China’s rapid expansion were made decades ago, and the national and international context has changed a great deal. Coal is no longer clearly the cheapest source of energy in China.

In fact, this was not even clear when China’s industrialisation took off. Nuclear power was, on average, cheaper than coal in the 1990s. Coal’s historic dominance in China likely resulted from it being a large, domestically available, state-controlled resource, rather than considerations about the cost of electricity.

Coal-based generation capacity continues to be added in China at a dangerous rate, but the pace has halved since its peak in 2006.

Renewable electricity is rapidly becoming cost-competitive with coal, and mounting public concern about the wider social, environmental and human costs of the latter has reinforced renewables’ attractiveness. Mortality from air pollution in China (mainly from coal-burning) is valued at 10% of its GDP. The government has now adopted air pollution laws that will only permit the most expensive technology with the most up-to-date pollution control devices. Three Chinese cities have banned new coal plants altogether and all major plants in Beijing are being closed down.

Given China’s enormous supply of domestic, secure and affordable renewable resources, it is safe to say that if China industrialised today, it is unlikely that coal would play as important a role in its energy mix.

Frequently asked questions

Doesn’t coal provide a valuable source of government revenue?

In countries with abundant coal resources, royalties and resource-rents theoretically have the potential to raise government revenue. But the track record is mixed.

Market fluctuations, environmental regulations and increased competition from renewables and natural gas are driving structural decline in some coal markets. The recently adopted Paris climate agreement reinforces these market signals. These factors make coal an increasingly unreliable source of government revenue.

In West Virginia, US, coal revenues have dropped from $1.2 million in 2012 to $100,000 in 2014, resulting in job losses and budgetary issues.

In addition, political pressure to support domestic production often leads to subsidies to prop up the industry, which can strain government budgets. In Colombia, for example, tax exemptions for extractive industries cause the government to get little, if any, revenue from the sector.

The OECD estimates global coal subsidies amounted to $6.1 billion in 2014. Factoring in the costs of coal-induced air pollution and climate change, the IMF estimates that the wider societal costs of coal subsidisation amounted to $3.1 trillion, or 3.9% of global GDP in 2015. On top of this, public finance for coal projects in the form of government-backed loans, export credits and guarantees is estimated to equal $9 billion annually.

Some coal companies are also known to actively avoid paying royalties and taxes. Through illegal exports of coal in Indonesia, companies avoid paying an estimated $4 billion annually in royalties. In Australia, Glencore moved $9 billion in sales to ’related parties’ offshore in 2014, enabling it to record a loss of $1.4 billion and exempting it from paying taxes on its profits.

A lack of transparency in government and coal industry accounting makes it difficult to analyse the overall distribution of public and private costs and benefits from coal mining. However, the shrinking of the global coal market, combined with the costs of subsidisation and government expenditure needed to deal with coal’s impacts on public health and the environment, makes coal a poor bet for government revenue.

Frequently asked questions

Shouldn’t countries with abundant coal resources use them for domestic power needs?

In countries endowed with large domestic reserves, coal historically offered a relatively inexpensive source of electricity from a secure domestic resource, particularly when the environmental and health impacts of coal went unmeasured or ignored. As outlined above, however, most of these countries are also endowed with other energy resources that are attractive today even without taking into account the costs of subsidies and the environmental and health costs of coal.

South Africa, for example, has relied for years on its substantial coal reserves for energy, but the economics of coal have changed rapidly and politics will need to catch up with this new reality. Wind power was recently purchased by South Africa’s utility at prices 17% lower than those projected for the country’s two new coal-fired power plants, Medupi and Kiseli. In India, utility scale solar is similarly outcompeting new coal. When the costs of coal-induced air pollution, water pollution and consumption, subsidies, and the impacts of climate change are taken into account, the case for renewables is even more compelling.

As coal plants are long-lived assets, with a lifetime of 40 to 60 years, a rapid expansion of coal-based generation capacity also risks locking in dependency on dirty technology. Coal plants are increasingly at risk of becoming stranded due to regulations on air quality, water consumption or carbon emissions and competition from renewables. Indeed, these factors have already stranded coal assets in the United States and the European Union.

Coal’s high external costs and risks are tipping the balance in favour of alternative, renewable energy sources that also provide a domestic and secure energy supply.

Frequently asked questions

Shouldn’t countries with coal resources mine it for export?

Coal is abundant and easy to transport, while its mining is relatively free of geopolitical tensions (compared to other extractive sectors), making it an attractive export product. Yet market forces and regulatory action on air quality, water consumption and carbon emissions mean global demand for coal probably peaked in 2013-2014, creating serious doubts about future export opportunities.

Around the world, coal prices have spiralled in recent years, threatening the viability of coal mining companies. Moody’s Investors Service estimated that about half of the world’s coal output is already unprofitable.

Indonesia and Australia, the world’s two biggest exporters, hope markets will grow in Korea, Taiwan and Vietnam. Yet, increased demand in these countries is not expected to make up for reduced demand from China, India and Japan. Vietnam recently shelved plans for 70 large coal fired power plants (44GW) in a move towards cleaner energy.

The demand for coking coal has not been as affected, but its price too has fallen rapidly; rising demand in India is unlikely to offset declining demand in China.

With declining markets, capital for coal mining is drying up. In Queensland, the recently approved Carmichael mine has struggled to secure finance.

Even in the context of strong markets, the promise of fossil fuel resource-led growth has never been straightforward. The resource curse hypothesis suggests that an excessive dependence on exports of raw materials makes countries’ fiscal balances vulnerable to commodity price volatility. It further suggests that this dependency encourages rent-seeking behaviour and corruption, and that large inflows from foreign capital can lead to contractions in other sectors, such as manufacturing and agriculture (a phenomenon known as ‘Dutch disease’).

Climate change is posing an additional challenge to the resource-led growth model, strengthening the argument that government support for building new coalmines to export coal is poor economic strategy.

Frequently asked questions

Won’t phasing out coal lead to job losses?

Countries heavily dependent on coal often cite the risk that phasing out coal will result in heavy job losses. At the local level, this is a serious concern.

A coal phase-out would lead to the loss of specific types of jobs, like coal mining, that tend to be concentrated in particular communities and regions. It will therefore be important for governments and trade unions in these areas to plan proactively for a phase-out by compensating, retraining and supporting at-risk workers to make the transition to new jobs. To this end, the International Trade Union Confederation has launched a ‘Just Transition’ campaign, calling on governments to consult with trade unions and employers to ensure fair and effective transitions towards sustainable, low carbon societies.

Despite the risks to jobs in specific locations, it is incorrect to assume that a transition from coal will exacerbate overall unemployment. While some jobs will be lost, others will be created – including in the renewables sector.

Overall, renewable energy industries already employ more people than the coal industry. The World Coal Association estimated that the coal industry employs up to 7 million people. The International Renewable Energy Agency estimates that 7.7 million people were employed in solar, bioenergy, wind, hydro and geothermal industries in 2014 (see figure). In China and India alone, 3.4 million and 440,000 people are employed in renewable energy, respectively.

Renewables also create significantly more jobs than coal per unit of energy produced. Combined, wind and solar employ more than four million people, despite representing only 5% of the world’s electricity mix compared to coal’s 40%. As renewables gain a greater share of the energy mix, we can expect that overall employment in the energy sector will increase.

It is also important to consider what will happen to those jobs in industries that depend on energy. The impact of a coal phase-out on these jobs will depend largely on the structure of the economy and the types of production being powered.

Frequently asked questions

Don’t poor countries need coal to industrialise?

Previous questions have shown that to reduce extreme poverty, economic growth is needed in the sectors where poor people are employed – particularly smallholder agriculture and the informal sector. As economies develop, however, labour tends to move away from agriculture into other sectors. In industrialised nations, growth in the manufacturing sector was historically critical to creating jobs for the urban poor and building a middle-class; coal was often the energy source of choice. Some argue that similar coal-powered growth models will be needed in poor countries today.

Indeed, poor nations do need growth in sectors that create decent jobs for low-income groups. Whether this growth should be powered by coal is a different question.

As discussed earlier, numerous cost-competitive energy alternatives exist to power industrialisation.

Furthermore, it is no longer clear that poor nations will be able to emulate the energy-intensive industrialisation of the past – not because of climate change, but because of technological progress and the changing structure of the global economy.

New analysis from Harvard economist Dani Rodrik suggests cheap labour might no longer provide the competitive advantage it once did to enable industrialisation in poor countries. Increased mechanisation has substantially reduced manufacturing costs, even in developed economies. With globalised trade, many poor nations have become net importers of cheap manufactured goods from richer economies, undermining the development of their own nascent manufacturing industries.

'In the absence of sizable manufacturing industries, these economies will need to discover new growth models,’ Rodrik suggests. Alternative pathways to growth – such as services-led growth – will likely require less energy than historical models of industrialisation, further eroding the argument that coal is indispensable for development.

Regardless of the growth sector, more attractive energy sources than coal will generally be available to power it. A coal phase-out per se will not kick away the ladder to prosperity from poor countries.

Frequently asked questions

What do the environmental impacts of coal mean for economic growth and poverty?

The negative environmental and social impacts of coal mining and burning coal for power generation can damage the prospects for economic development overall, putting current and future poverty reduction at risk. Coal is the single largest source of the carbon dioxide emissions causing dangerous climate change, which threatens to undermine the productivity of global marine and terrestrial food production systems. Four in ten (44%) of the people most vulnerable to a changing climate are already surviving on the edge of subsistence. Globally, if left unchecked, climate change could help wipe out current gains and push up to 720 million people back into extreme poverty.

At the local level, coal’s environmental impacts are similarly damaging. Coal plants – particularly the sub-critical kind that are most prevalent in poor countries – are major sources of local air pollutants (PM, NOx, SOx and mercury). In India and China, 90% of subcritical plants are located in areas with air pollutants exceeding WHO guidelines. In India alone, emissions from coal are estimated to result in the premature deaths of as many as 115,000 people annually, including 10,000 children under the age of five. In addition, more than 20 million asthma attacks and 900,000 emergency room visits are linked to air pollution from coal. Poor people, minority groups and those living downwind of coal power plants are disproportionately exposed to these health risks.

The water consumed by subcritical coal power stations relative to the amount of energy they produce is second only to nuclear plants. Globally, nearly one-third of existing subcritical coal plants exist in water stressed areas. In China and India, this figure is more than half. Water stress is only projected to get worse, with demand projected to grow to more than double current supply by 2030.

The environmental and social damage caused by coal, with its knock-on impacts on economic growth and the livelihoods of poor groups, will be considered in more depth in our next FAQs.

These FAQs were developed by CAFOD, Christian Aid and ODI, with contributions from organisations working on energy and poverty issues in developing countries.

Partner organisations

![]()

Contributing organisations

![]()

![]()

![]()